Houston, We’ve Had a Problem

The Federal Reserve responded to the spectacular financial meltdown of 2008 by putting a bottom under the cascading financial prices. This was accomplished by buying, buying, and buying some more. Then when the downdraft of prices reached bottom, the Fed phased in additional largescale asset purchases with the intent of providing cash resources to banks in order to start the bank expansion and economic rebuilding process. This reduced interest rates to the most affordable of all times as a way to induce prospective borrowers to spend more money.

All told, the Fed buying spree increased its balance sheet assets from $ .8 to $4.3 trillion — an increase of 5.5 times. For comparison, a normal Fed buy over that time period would have increased its assets by only .36 times. When all the Fed’s buying power is deposited with banks, it results in bank cash reserves in excess of the minimum required from which the banking system can ramp up credit by some multiple.

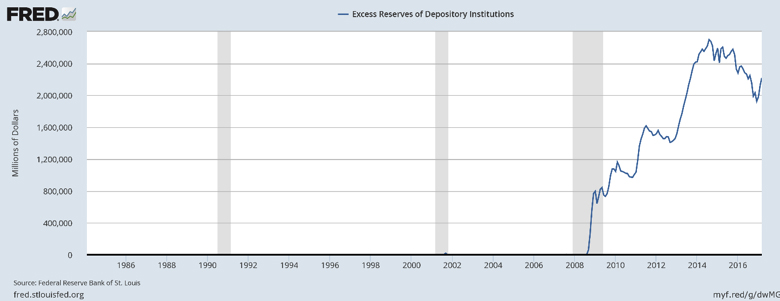

To give you can idea of how extreme this was, the graph below shows the excess cash reserves that banks held from 1985 through 2016. This is the base upon which banks can build lending some multiple of the excess cash. Before 2008, excess reserves were essentially zero. After 2008, they went into orbit.

Nearly nine years later, there has been an economic uplift — but it has been disappointing. The economic growth rate reached approximately half the growth rate it had formerly been capable of, which appeared to reduce the unemployment rate to the 5 percent target. But this reduction was made easier as the population’s labor participation rates have been dwindling.

Even so, the Fed has claimed bragging rights for a successful economic “save,” but it still left interest rates too low to take care of its other “constituency”: Baby Boomer investors in need of a yield on (relatively) safe fixed income in order to finance their retirements, either from their savings or by way of their pension funds, insurance annuities, etc.

So for that constituency to “get theirs,” the Fed’s Normalization Plan calls for raising interest rates and cutting its own balance sheet down to size. This implied selling of Federal Reserve owned assets would sop up excessive commercial bank cash reserves. And that would prevent low interest rate bank loan expansion.

Thus, large scale selling not only sops up cash but also puts downward pressure on market determined bond prices and upward pressure on market yields, both in the open market and at the bank loan counter. It’s enough selling to absorb almost all of the remaining excess cash on bank balance sheets so that banks thereafter would be restrained from advancing credit.

This is a reversal of Fed expansion in which the Fed buys assets with new money to fuel commercial bank lending. The last three generations of macroeconomic students worldwide might recall that this went under the name “the money supply multiplier.”

So in a general sense, you can see that putting monetary policy in a serous reverse course raises the question of can a tepid economy continue its relatively slow motion advances?

Formerly, this is the sort of thing that was done in a far less aggressive form when the Fed set out to restrain an economy that was generating inflation. But today, there is no runaway inflationary dog that needs to be reined in with a tight leash, a la Paul Volcker.

What is also concerning about the tight leash is that it’s being used at a time when the new G-20 Basel liquidity requirements (meaning banks must hold more cash) are being imposed on the banks of the G-20 countries. So cash just sits on bank balance sheets and can’t be used to ramp up lending because it’s being used to fulfill those liquidity requirements.

As described in “It’s a Whole New Monetary Ballgame,” we now have duel cash regulations imposed on banks. (Just what the banks needed, more regulation!) They have both their own domestic regulatory apparatus of required cash reserves and the G-20 regulations from Basel, Switzerland.

So the removal of bank cash via “Normalization” comes at a time when the banks already need to place cash on hold to satisfy Basel’s rules. That surely suggests a constraint on bank loan growth.

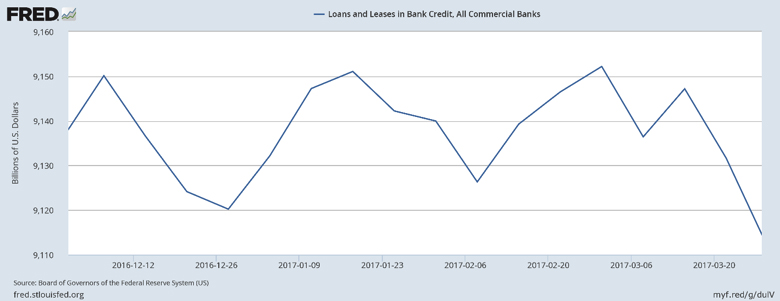

And this indeed is what has occurred over the last four months. Bank loan levels (seasonally adjusted) are shown below.

So the Basel liquidity requirements are a leading theory of why the slowdown of bank lending is occurring. At this point, though, that’s only a guess because the actual amount of cash required to satisfy Basel is based on each individual bank’s 30-day cash needs during a financial crisis as determined by an annual regulatory audit — but that’s not released to the public.

Whether or not this new cash requirement is deterring bank loan growth, it’s not consistent with maintaining economic growth, and it’s likely to cause a “Houston, We’ve Had a Problem” moment for the Fed.

If you recall, those words were transmitted from Apollo 13 to Mission Control in Houston in 1970. As the flight crew approached the moon, they heard a loud pop, and the command module of Apollo 13 subsequently began losing oxygen. This, in turn, required the crew to reverse course and attempt a death-defying return to Earth. The question is, will the Fed similarly be forced to reverse course after years of planning for normalization? Because it appears that banking lending is losing oxygen.

If so, there will be consequences for an already tarnished Federal Reserve that has fallen from esteem in the eyes of the market, Congress, and perhaps the administration. So the best laid plans to get to the moon — or, in this case, to bring central and commercial banks back to normalcy and land the economy safely with higher interest rates — has a reasonable chance of being scuttled.

So there are far more questions to this story than answers. Stay tuned to find out whether the monetary version of Apollo 13 lands “normally” with smaller balance sheets and higher interest rates while maintaining economic growth, or whether the Fed is forced into a humiliating about-face that requires it to maintain its easy money profile until the economy can be made to somehow grow on its own without monetary excess.

In order to go back to monetary and interest rate normalization, we need the economic responses that the new administration is tinkering with to unleash economic growth as we used to know it.