The antidote to a troubled macro environment since Keynes wrote the book in the 1930s has been the dual demand-side sledgehammers of government deficit spending and monetary expansion.

The antidote to a troubled macro environment since Keynes wrote the book in the 1930s has been the dual demand-side sledgehammers of government deficit spending and monetary expansion.

Both were thought to induce private spending with multipliers that would generate output and absorb the unemployed. Well, that’s how the theory went.

When it was first applied, it was not a theoretical experiment but rather the necessity of paying for and financing WWII.

At that time, the twin necessities of fiscal and monetary policy jolted the economy forward with such force that the unemployment rate was driven down to 1.2%. It appeared to provide validation of what fiscal and monetary policy could do, and economists and policymakers around the globe embraced it (and they still do).

After all, it simply required legislation for spending, raising the debt ceiling, and the Fed’s Open Market Committee’s agreement to go along with it. Basically, it was Bureau of Engraving and Printing policy that printed both the Treasury securities to pay for the deficit spending and the dollars to purchase them.

It was the easy way out, which became Plan Ain times of economic distress, whether they’re related to shortfalls of income or jobs. And now it’s also intended to rebuild wealth, save banks, and cheapen the dollar as well.

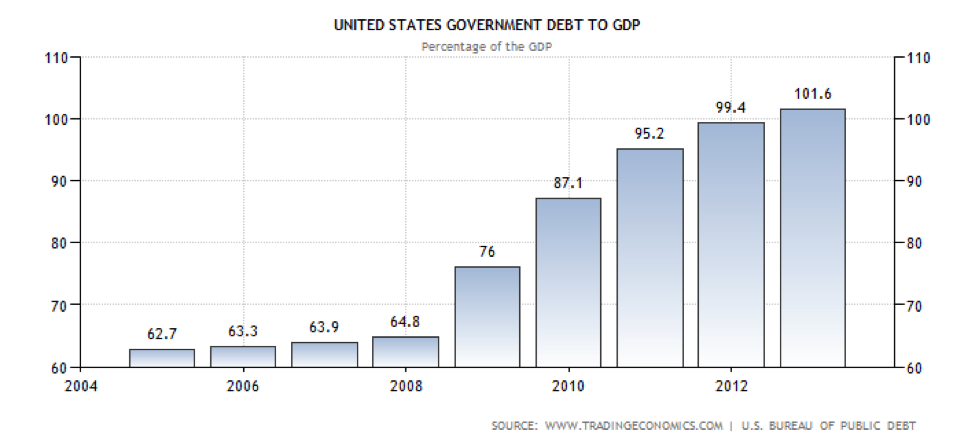

But for these macroeconomic sledgehammers to work, they are not cheap. US Government debt to GDP has increased from 62.7% to 101.6% in the last eight years. The relative size of the Fed’s wartime quantitative easing was a 50% expansion of its balance sheet — as opposed to a 300% expansion in the modern day reincarnation of QE. But alas, unemployment has been driven down to but a narrowly measured 6.7%.

So it’s obvious that something else is afoot, and it has to do with the question of why the twin sledgehammers are not working as well anymore. And furthermore, what is the “something else” that policy makers are now turning to? That is to say, what is Plan B?

The basic answer to why the sledgehammers are not working is that both monetary policy and fiscal policy are debt-financed spending, either by the government or the private economy. The problem is that it works as a cyclical remedy, as long as the debt doesn’t accumulate — which implies that in the prosperities that follow, debt reduction should take place. That is what George W. did not do, but Bill Clinton did.

The need to avoid accumulating debt was forgotten as the economic high just induced a greater desire for prosperity with mindless expansion of the debt-to-income ratio.

Basically, debt-driven spending — whether public or private — is a cyclical policy that is not meant to be a long-term secular fix. If a government and the Fed keep at it as a secular fix, it has offsetting effects when a greater share of income is required to service debt.

This is not lost on the private economy, as consumer debt relative to income has been worked down since it peak in 2007, which in turn continues to slow the economy today. Nor was it lost on Keynes himself. But governments didn’t get the memo, and they keep on piling up debt, which restricts the economy by creating a need for more revenues to service that debt.

The twin forces of stimulus from debt-financed spending and the subsequent need to service or retire debt is becoming evident today. As an example, in Japan since the last election, Abonomics has employed the macro sledgehammers with great force but has followed up with a national consumption tax that offsets Plan A. Much the same is happening in Europe and in the U.S. with QE tapering and fiscal sequester reining in the expansion of Plan A.

So what becomes Plan B when Plan A is being made to face the facts — specifically that secular debt accumulation is ultimately counterproductive?

Politicians are now doing what is pragmatic to attract business to their geographical location without the benefit of Ivy League economic theory. This is being done city against city, state against state, and now country against country. Plan B at the country level was the subject of the recent G-20 meetings as a response to the Fed’s tapering of QE, so it’s going global.

Plan B takes the form of reducing taxes as compared to your competitor, enacting less costly and burdensome regulations, and even underwriting business start-up expenses. It also takes the form of job training and infrastructure development. Those and other efforts are supply-side efforts to be relatively more competitive.

Some of them are outliers by historical example. That would include Michigan, which became a right-to-work state in 2012, and others in the Midwest are following.

There is a significant difference in the public perception of Plan B as compared to Plan A. In B there is little accompanying press and no photo opps for the politicians or the Fed Chairman, and hence fewer images to drive Wall Street expectations. But these low-profile policies are relentless, albeit slow. On the surface they appear to be policies that do more in totality than merely change the location of business. The benefits come in the form of greater efficiency (measured by output per worker) and less debt accumulation, either public or private.

Are they enough to offset the unintended debt consequences of previous demand stimulus? That we shall see, but at least this is a move in the right direction toward offsetting the ill effects of secular debt accumulation.

A major question is: Can these policies that are associated with the Right Wing be implemented by Left Wing majorities in many places? Well, if Liberals are in political control, they are also responsible for economic outcomes. So they will find ways to implement typical conservative platforms packaged as inspired liberal genius.

Sign up to receive the Spellman Report. Bracing financial and economic insight. Now with free delivery!

has been applied in heroic proportions, the employment high ground of five years ago has not been revisited. This graph clearly reveals this recovery lags all others in the post WWII era in which stimulus spending was considerably lower.

has been applied in heroic proportions, the employment high ground of five years ago has not been revisited. This graph clearly reveals this recovery lags all others in the post WWII era in which stimulus spending was considerably lower. of children aged 4 to 6 by Stanford psychologist

of children aged 4 to 6 by Stanford psychologist