Every financial debacle that takes banks down is an open invitation for governments to impose regulation with the aim of preventing a reoccurrence. The financial crisis of 2008 was no exception.

Unfortunately, revisions in the banking environment generally end up with unintended consequences, and they are far-reaching.

The regulation in question are designed to reduce a banking system vulnerably to being caught with insufficient liquidity in a market-driven flight to cash. (It’s something that Deutsche Bank no doubt should be thinking about at this time.) All this is explained in Part 1 of The New Monetary Ballgame, which is a deep dive for those most interested.

But in brief summary, the Bank for International Settlements (BIS) — the central bank for central banks — is imposing liquidity and solvency criteria on the banks for all member countries of the G-20. This is being imposed because the financial crisis of 2008 was worldwide, and now all member governments have accepted the BIS’ dictates.

The immediate thrust of these regulations is to impose substantially higher liquidity requirements on banks. The purpose is to allow banks to retire all bank claimants who want out if a bank run à la 2008 were to occur. Liquidity means being prepared with cash. And if not, banks are forced to sell assets en masse. This could create a far-reaching financial selling crisis, which in turn forces governments into the financial rescue business.

In this new monetary ballgame, banks can choose from a menu of assets set out by the BIS to satisfy the new and higher liquidity requirements. Obviously, cash on hand or deposited with a central bank (not necessarily their own) qualifies. In addition, the BIS wants these assets to be interest-bearing so as not to sacrifice bank profitability in the quest for more liquidity. As a result, some marketable interest earning assets also qualify for the liquidity requirement. But which?

In general, the preference is for banks to hold interest-earning assets for which there is a robust secondary market that could turn those assets into cash with little discounting during a financial crisis.

This narrows the potential candidate assets very quickly because most assets substantially decline in value in secondary markets in the midst of a financial crisis. Hence, what banks need in a selloff is what market traders refer to as “flight to quality assets.” In regulatory jargon, this is now being expressed as High Quality Liquid Assets (HQLA).

Certainly highest in the pecking order among HQLA would tend to be sovereign bonds and perhaps highest quality corporate or muni bonds, with the regulators permitting.

And that is the way the discussion rolled out with the European members nominating their own country bonds to be considered HQLA.

But you can image what followed when, for example, Greek sovereign bonds with a Moody’s Rating of Caa3 would have become eligible to meet the HQLA requirement. As could be expected, the US objected. In its opinion, only US Treasury securities qualify to be HQLA for all countries’ banks.

While on the surface this appears to be an argument about bond quality, at the Machiavellian level this is an argument over whose bonds will be imposed on the banks of all the G-20 countries. Result? The US won. Banks from all G-20 countries can now satisfy their BIS liquidity requirements by holding US Treasuries.

So when the global bank regulator can, under the guise of “safety and soundness,” impose an incentive to hold US Treasury obligations, it has established a mechanism to finance US government debt at lower yields than would otherwise be the case. That comes just in time if you ask me, as the US structural deficit has widened to $0.6 trillion/year with decades of rising baby boomer entitlements staring us straight in the eye.

So you can see the advantages involved from winning the Machiavellian jostle and be deemed, the king of sovereign debt issuers. The US sovereign bond prices will be higher and the yields will be lower. Indeed, over the summer, the 10-year US Treasury yield fell to its all-time low of 1.37% just as banks across the G-20 were approaching the September 30th deadline to fulfill their new liquidity requirements.

In comparison, the BIS allowed US investment corporate grade debt to be counted as bank liquidity but with only a 50% weight. That is to say, anticipate that corporate debt would sell in the market during times of stress at a 50% discount. Not bad when you realize that even investment-grade US municipal bonds receives a haircut of 100% in the calculation of its contribution to bank liquidity. Thus municipal bonds clearly lost out in the Machiavellian jostle as none of it counts for bank liquidity.

As a result of this weighting, the market yield spread has widened between assets classes such as US Treasury bonds and investment-grade muni bonds. With muni debt having less regulatory value, their yields have risen relative to those of the US Treasury that does have regulatory value.

What is yet to come over the next two years is higher ratios of equity capital for commercial banks. This means banks will need a larger amount of their own banks’ stock on their balance sheet to increase their net worth and ability to take asset losses without going insolvent.

But every additional share sold dilutes existing stockholders’ claim on banks’ profits. When substantial increases in bank equity capital need be raised, especially at times of very low market pricing of bank equity, it will take a lot of shares at low prices to raise the required amount of additional bank capital. This will dilute existing shareholders into a nothingness.

But in this rigged game, there is an alternative to bank stockholder dilution: Hold larger proportions of US Treasuries as assets and, since they are anointed by the regulatory to be “riskless,” a bank has less need to protect itself from losses as the regulator claims those assets will not deteriorate in value. Hence, the regulatory mandate for higher equity capital is waived against those assets by holding more US Treasury obligations!

The result is that yet more G-20 country banks, especially weaker European banks, will add to their holdings of US Treasuries rather than dilute their existing stockholders via the sale of a ton of additional bank stock.

It’s so obvious, one doesn’t need to take a step backwards to get perspective. When assets must be bought and held by developed world banks which are a very large asset pool (a multiple larger than central bank assets), it generates considerable demand for that asset that doesn’t go away. It becomes a rigged game because the price of the issuers’ debt is supported in the market and the issuer’s borrowing costs decline.

In turn, it encourages the subsided issuer to keep issuing more debt.

Therefore, it’s no great surprise that we find ourselves at a point where the developed world countries are talking about issuing yet more country debt and spend the proceeds as the way to generate more aggregate demand. This would constitute a shift toward fiscal policy and away from monetary policy to manage a depressed economy.

Another major implication is that the textbook treatment of interest rate determination based on investor queasiness from inflation and default still remain. But those influences on interest rates pale by comparison to the fiat demand generated by G-20 commercial banks for US Treasury securities.

Stay tuned. It’s a new ballgame, and we’re going to have to relearn many of the things we thought academics and history had taught us.

Click to Email Dr. Spellman

Is their loyalty to government subsidization above their responsibility to their own central banks’ balance sheets and the commercial banks they regulate? Or are they fools who have been seduced by Keynesian central bank ideology in which lower interest rates are seen as always better for the economy? And that includes

Is their loyalty to government subsidization above their responsibility to their own central banks’ balance sheets and the commercial banks they regulate? Or are they fools who have been seduced by Keynesian central bank ideology in which lower interest rates are seen as always better for the economy? And that includes

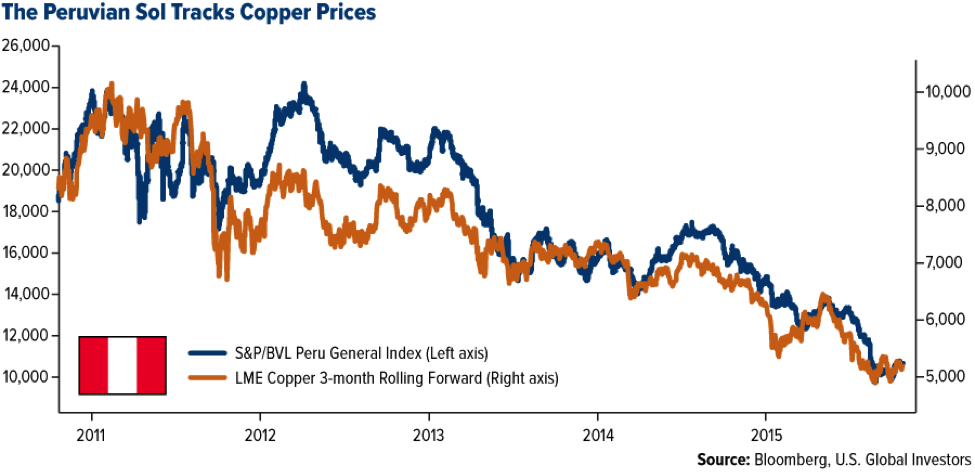

Foreign capital provides jobs and income, but it becomes problematic because it is seldom applied at a steady and measured pace in proportion to the opportunities. During the Great Recession, the Fed’s QE provided investors with a large liquidity pool disproportionate to the onshore investment opportunities, so a good deal of that liquidity gushed into off-shore investment. And much of that went to the commodity and energy industries, which, at the time, were supply-constrained and expensive. These include Brazil, Indonesia, Russia, South Africa, and Chile, Peru among others, as well as some developed country plays in Australia, West Texas, and Canada. In investment booms fed by outside (and not very discerning) capital, animal spirit-driven developers keep on borrowing and building to be absorbed by the market before their competitors, and the unrestrained booms that follow result in over-building, excess production, inventory build-ups and in turn soft prices, debt defaults, eventual bankruptcies, and penny stocks. That much is true for any domestic boom and bust, but now there is a foreign twist when the projects are debt-financed from offshore sources that typically require repayment in US dollars. Hence, foreign-financed investment has a built-in currency crisis in the making when settlement takes place because it drives the price of the US dollar upward and the local currency downward. Predictably, it comes at a time when the boom is over-built, leaving investors scrambling to generate revenue, and commodities continue to be sold at very low prices in order to cover the rising cost of dollar-debt repayment. There is a rush to extinguish dollar debt before a property is lost to foreclosure, which, in turn, leads to major multiple market reactions – all downward. The selling of commodities at ultra-low prices creates an adverse currency movement for the affected country. For example, see the correlation (below) of the declining price of copper relative to Peru’s Sol and Iron Ore relative to the Australian Dollar.

Foreign capital provides jobs and income, but it becomes problematic because it is seldom applied at a steady and measured pace in proportion to the opportunities. During the Great Recession, the Fed’s QE provided investors with a large liquidity pool disproportionate to the onshore investment opportunities, so a good deal of that liquidity gushed into off-shore investment. And much of that went to the commodity and energy industries, which, at the time, were supply-constrained and expensive. These include Brazil, Indonesia, Russia, South Africa, and Chile, Peru among others, as well as some developed country plays in Australia, West Texas, and Canada. In investment booms fed by outside (and not very discerning) capital, animal spirit-driven developers keep on borrowing and building to be absorbed by the market before their competitors, and the unrestrained booms that follow result in over-building, excess production, inventory build-ups and in turn soft prices, debt defaults, eventual bankruptcies, and penny stocks. That much is true for any domestic boom and bust, but now there is a foreign twist when the projects are debt-financed from offshore sources that typically require repayment in US dollars. Hence, foreign-financed investment has a built-in currency crisis in the making when settlement takes place because it drives the price of the US dollar upward and the local currency downward. Predictably, it comes at a time when the boom is over-built, leaving investors scrambling to generate revenue, and commodities continue to be sold at very low prices in order to cover the rising cost of dollar-debt repayment. There is a rush to extinguish dollar debt before a property is lost to foreclosure, which, in turn, leads to major multiple market reactions – all downward. The selling of commodities at ultra-low prices creates an adverse currency movement for the affected country. For example, see the correlation (below) of the declining price of copper relative to Peru’s Sol and Iron Ore relative to the Australian Dollar.

This strong currency decline then causes unrelated companies, individuals, and even governments to sell most anything denominated in local currency and use the proceeds to purchase US dollar-denominated assets. The debt repayment wave deteriorates into a generalized capital flight and a currency collapse for the involved country. Basically, the bright shining buildings shown above are still standing and shinning, but in the economic and financial dimensions, all prices are falling down. This is the basic scenario that followed the early days of globalism in which there was an over-build of manufacturing capability in the cheap labor countries of Asia in the 1990s. The consequence was a bust phase known as the

This strong currency decline then causes unrelated companies, individuals, and even governments to sell most anything denominated in local currency and use the proceeds to purchase US dollar-denominated assets. The debt repayment wave deteriorates into a generalized capital flight and a currency collapse for the involved country. Basically, the bright shining buildings shown above are still standing and shinning, but in the economic and financial dimensions, all prices are falling down. This is the basic scenario that followed the early days of globalism in which there was an over-build of manufacturing capability in the cheap labor countries of Asia in the 1990s. The consequence was a bust phase known as the

and act on the regulatory reports or what is the dollar cost of corporate and personal compliance to regulation? Does that make the argument?

and act on the regulatory reports or what is the dollar cost of corporate and personal compliance to regulation? Does that make the argument?