Tension is building among stock investors.

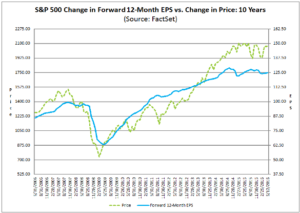

Stock prices have levitated, but the most fundamental determinant of stock price support — an uplift in corporate earnings — has gone soft. The S&P 500 earnings actually declined 7.1% year-over-year and the US and moreover global economies that support it are sputtering on all cylinders.

Additionally, given the economic recovery from the Great Recession’s lows, wages are rising modestly — but with zero productivity, there is not much to offset these costs suggesting that profit margins will not hold up.

This comes on top of a seven-year run of stock prices that has outpaced the recovery of corporate earnings (as shown below), making for a relatively high price/earnings ratio as compared to historical benchmarks. All this concerns stock mavens and for good reason.

But on the other side of the ledger is the resolve of the central bank to provide a wealth effect for consumers to keep on consuming. While it’s quite clear that ultra-expansionary monetary policy carried out via bond purchases has elevated bond valuations and, in turn, produced low market yields, what support does monetary policy have for stock prices?

Since the onset of Fed QE, there’s been a relationship between the money base and a broad stock price index (see below), but what’s the link that caused them to move together- as they have?

First, and most fundamentally, a central bank purchase of bonds from private parties is financed by new money. Hence, the other side of the bond purchase is liquidity in the hands of a portfolio manager, who then scans the financial landscape for a replacement asset that includes stocks. This is the process by which bond buying, paid for with new money, ripples out to affect prices of other assets.

From there, internal portfolio dynamics lead to increased stock purchases in the following way. When bond appreciation generates a wealth effect for investors’ portfolios (particularly institutional investors), then managers must re-balance assets and, in the process, redistribute the bond gains to other risk assets not purchased by the Fed.

Institutional rebalancing is further motivated these days when ultra-low-yield bonds create pressure to generate investment income somewhere else in the markets. This hunt for investment income can take the form of stock dividends or stock appreciation, both of which have generated total returns over the last seven years.

This is say, there is pressure to switch to assets that have become known as “alternatives,” and this has included equities, real estate, and (for a time) commodities. In essence, income investors have become bond migrants who have been forced from their preferred habitat to other asset classes.

However, there is a simpler way to look at this process of spreading out the price increase. There is a cross-elasticity of demand among alternative assets in a portfolio — much like when a government supports meat prices, the price of fish also rises, even though the government didn’t actually buy any fish. This occurs because the expensive meat drives consumers to purchase more fish, which in turn causes fish prices to increase as well.

To an economist, this so called cross-price elasticity of demand, causes more intensive buying of substitutes when one item becomes expensive.

Another factor that leads to stock demand and levitated prices is a lower discount rate in the market. Institutional investors are not indifferent as to when income arrives: they discount future income to present day terms by discounting at the rate that could be earned on the asset if it were in-hand today — that is, what they are giving up when income arrives later in time.

In this regard, eight years of depressed yields has likely caused the discount rate applied to future earning to be reduced, which, in turn, causes the present value of future income to rise.

As an example, for a single dollar of corporate earnings that is projected to arrive in 10 years, if discounted by today’s low yields of 2%, would have a present value of 81 cents, whereas the same dollar discounted at a 5% rate would, in present value terms, be reduced to 62 cents. Hence, lower market yields boost the valuation of future income even if the future income is not projected to grow. In this case, there is a 31% increase in today’s value for 10-year out income when yields fall as far as they have.

The ultra-low interest rates further work to support stock prices as they induce companies to issue bonds with low yields and apply the proceeds to purchasing their own equity shares. While this doesn’t generate future corporate income, it does increase income per share and enhance stock prices as long as investors ignore adverse effects from a more leveraged future.

Equity share repurchases recently got a further boost when the European Central Bank took up the practice of purchasing corporate bonds at issuance, even for Euro subsidiaries of US companies. This is likely to add to the pool of additional buy-backs of US-issued company stock. And why not when McDonald’s was able to place a 12-year maturity at a .75% rate that would make the US Treasury Department envious?

Last, in this description of stock price levitation, one should muse on the thought that maintaining stock prices at high levels has occurred despite an absence of Fed bond purchases since October 2014.

While foreign central banks keep at it (and, in the case of Japan and China, actually purchase stocks in addition to bonds), something else must be providing stock price support in the absence of additional Federal Reserve buying.

Not much thought has been given to relative scarcity as a result of bonds being purchased by central banks and stock being purchased by the issuing corporation. These assets will not see the light of day again as there is no way for them to be offered (without a change in policy) on secondary markets.

Hence, with stock and bond issues being locked up, relatively higher prices do not elicit as much of a supply response that would reduce market prices. The historical description for this is a market “cornering,” implying control over price from collecting a significant proportion of an asset — and the central banks are cornering the government bond issues. Thus scarcity allows prices to continue to be levitated thought the Fed buying has stopped.

Indeed, with this in mind, the central banks have vowed to purchase no more than 70% of any government bond issue so as to allow some private suppliers to establish a market price without being able to put much of a dent in its level.

All this is not to say that the unease felt by the stocks mavens can’t bring more supply to the market than the bond migrants will absorb if their expectations go sour.

This would push stock prices downward. But the pent-up demand by the bond migrants for stocks, together with relatively more scarce corporate shares, has changed what we think of as the fundamental yardstick for pricey risk assets.

Thus, historical stock P/E ratios as a metric for an expensive market needs revision, as we are in a whole new history of a higher ratio of money relative to asset values along with more restrictive supplies of both high quality bonds and stocks.

Sign up to receive the Spellman Report. Bracing financial and economic insight. Now with free delivery!

Click to Email Dr. Spellman Economic growth in the developed world is falling well short of the post-WWII experience, and there are identifiable causes.

Economic growth in the developed world is falling well short of the post-WWII experience, and there are identifiable causes.

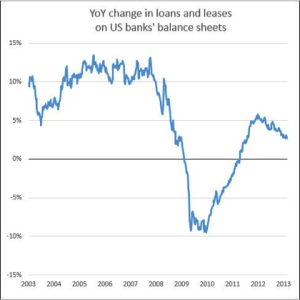

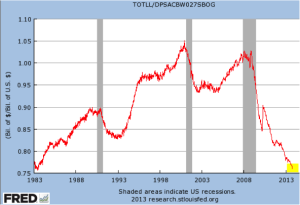

rate of the Fed’s QE. This rate of credit expansion by all sources is found in the Federal Reserve

rate of the Fed’s QE. This rate of credit expansion by all sources is found in the Federal Reserve  finance the same lending and spending outcome via the non-bank banks and the securities market.

finance the same lending and spending outcome via the non-bank banks and the securities market. A printing press is a handy thing to have. When a government or central bank can fund itself with money or claims on money, it can buy a lot of things and solve a host of problems, all without the need to tax. I wish I had one.

A printing press is a handy thing to have. When a government or central bank can fund itself with money or claims on money, it can buy a lot of things and solve a host of problems, all without the need to tax. I wish I had one. So as we approach the target unemployment rate without much economic recovery, the question is, can and will the target be redefined to be the unspoken necessity of supporting Treasury debt obligations?

So as we approach the target unemployment rate without much economic recovery, the question is, can and will the target be redefined to be the unspoken necessity of supporting Treasury debt obligations?  Today there is a de facto peg already in place. It goes under the title of zero interest rate policy (ZIRP). It is also known as financial repression, which includes ZIRP along with positive inflation causing real yields to go negative all the way out to almost 20 year maturities and has become the explicit policy of the Japan and implicitly of Europe as well.

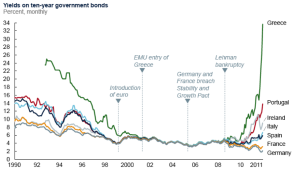

Today there is a de facto peg already in place. It goes under the title of zero interest rate policy (ZIRP). It is also known as financial repression, which includes ZIRP along with positive inflation causing real yields to go negative all the way out to almost 20 year maturities and has become the explicit policy of the Japan and implicitly of Europe as well. These are epic times in the developed world’s attempt to deal with the implications of government and consumer over-indebtedness. A general unshakable malaise has set in due to sluggish spending and a deleveraging banking sector, and as a result, employment growth is suffering. Governments in turn are faced with diminished tax yields and deficits remain bloated. As shown in Europe, ultimately they run out of willing buyers of government debt.

These are epic times in the developed world’s attempt to deal with the implications of government and consumer over-indebtedness. A general unshakable malaise has set in due to sluggish spending and a deleveraging banking sector, and as a result, employment growth is suffering. Governments in turn are faced with diminished tax yields and deficits remain bloated. As shown in Europe, ultimately they run out of willing buyers of government debt. from abroad.

from abroad. And some believe it will keep going. The price of the U.S. Treasury 10-year bond recently reached an all-time high, generating yields at all-time lows. Moreover, the market yield on the British perpetual bond is reportedly at a 300-year low. Bond mania has even spread to the sovereign debt of Denmark and Singapore and others where negative yields exist. More astonishing is the ability of France to issue short-term sovereigns with negative yields!

And some believe it will keep going. The price of the U.S. Treasury 10-year bond recently reached an all-time high, generating yields at all-time lows. Moreover, the market yield on the British perpetual bond is reportedly at a 300-year low. Bond mania has even spread to the sovereign debt of Denmark and Singapore and others where negative yields exist. More astonishing is the ability of France to issue short-term sovereigns with negative yields! Depression era came to an end with the onset of World War II, as shown in the chart to the right.

Depression era came to an end with the onset of World War II, as shown in the chart to the right. (That being said, it leaves open the question of whether intentional inflation is bravado in the absence of bank lending, which will be addressed in a subsequent blog.)

(That being said, it leaves open the question of whether intentional inflation is bravado in the absence of bank lending, which will be addressed in a subsequent blog.)