As a result of the 2008 financial meltdown, The Bank for International Settlements (BIS) was tasked by the G-20 countries to change the global rules of commercial banking in order to prevent a re-occurrence. Their mandate was: no déjà vu again, if you please.

The snuffing-out of future financial crises comes via regulation, and because regulation tinkers with the equations of the “system,” it changes the built-in reactions. This requires us to rethink what we presume will occur.

For example, it turns out that when the BIS tinkers with things to make banks more resilient to meltdown, it also makes them more resilient to monetary expansions. So this explains, in part, why even though the Fed increased its balance sheet by 500% since 2008, US commercial bank balance sheets have increased by only 45%. And since commercial banks provide credit directly to businesses and individuals, the (lack of) banking and in turn economic expansion has disappointed most observers — including the Fed itself.

Before getting around to explaining how that can happen, first, some background on the dynamics of a bank meltdown. This will provide you with an understanding of what the regulators are tinkering with and why, and then what the consequences will be.

Bank runs follow a typical scenario, and 2008 was a classic example. It starts with a loss of confidence in the banking system’s assets sufficient to cause bank depositors and other providers of short-term bank funding (deposits and loans) to exercise their right to exchange their claims on the bank for immediate cash.

This, in turn, forces banks to sell assets into the market to obtain cash in order to be able to “cash out” these bank claimants. The selling of bank assets must meet the pace of the demanded cash, and if the depositors and lenders aren’t mollified, it can turn into an asset fire-sale in order to obtain the needed cash quickly.

Cash is king in a bank run, and banks in need are willing to swap assets at a discount in order to obtain it — which is what causes a banking crises to become a financial crisis. These twin crises are two sides of the same coin.

It quickly occurs to depositors and claimants (even those affiliated with banks thought to be “solid”) that their banks’ assets are being compromised in market value by these fire-sales. This, in turn, causes the depositors of the “solid” banks to become jilted out of their comfort zones and to demand cash as well — just in case.

From there, the run affects those banks thought to be doing well.

Note that the first sparks in the financial meltdown are due to obtaining liquidity, but it quickly turns into a question of “is my bank still solvent?”

Solvency is the basic issue of whether my bank’s assets now exceed its liabilities so that it can cash out all claimants if need be. If not, the regulator might even beat the depositors to the punch and seize the bank in anticipation of an insolvency, which they can do. And they can be quick on the trigger because they suffer the residual losses if they guarantee the bank’s debt.

In that case, claimants then worry whether the resolution and liquidation of the bank calls for their claims on the bank to be bail-out or “bailed-in,” with the latter occurring more frequently these days. All this increases the uncertainty and fear by bank claimants as to whether they will be made whole. This then increases their propensity to more quickly cash out their bank claims when questions of illiquidity or insolvency arise.

For any reader that saw The Big Short, this should sound familiar. That movie depicted the moment in 2008 when investor and regulator focus turned to the solvency of Bear Stearns. Its stock price went into free-fall, and its claimants wanted their cash back. It was immediately over for Bear Stearns (forced merger with JP Morgan Chase), and the only remaining question as a claimant was, would you be bailed-out or bailed-in?

So it’s with this background that one could imagine the importance of reducing the vulnerability of the trifecta of risks: bank runs, financial meltdown, and an economy that gets sucked down by the implosion of the market value of wealth.

As you now see, bank and financial crashes are the result of depositors running to cash out, so perhaps you can imagine what the BIS is requiring of banks in the G-20 countries: Hold a higher proportion of cash or assets that can quickly be sold with little discount in a period of financial distress.

These requirements are spelled out in the new lexicons of banking called Liquidity Coverage Ratio or LCR. It defines the amount of cash and cash-type assets that banks must hold. The LCR is specific to each bank and is intended to cover the bank’s 30-day forward net cash needs in the course of doing business under financial stress.

To have adequate liquidity in financial distress, there is a greater emphasis on cash as the asset of regulatory choice, so there is no need to actually sell an asset to obtain cash during a financial crisis. Actually, the emphasis is even more narrow on cash in excess of what banks would be required to hold under country-specific banking laws.

It turns out that holding excess cash deposited with a central bank has great appeal to the banks as well to satisfy its BIS liquidity requirement. But let’s be clear: For the cash to be available to cash out a bank’s claimants, it must be in excess of the minimum cash amounts that country banking laws already requires banks to hold.

The BIS liquidity requirement is on top of the Fed’s cash requirement.

But there is a problem with holding excess cash to meet the liquidity requirement. In several G-20 countries, excess cash deposited at its central bank has a net charge called a negative deposit rate. For example, the European Central Bank deposit rate for its banks is -40 basis points, and marginal excess reserve deposits in Japan are at -10 basis points. The required liquidity comes at a high cost because negative deposit rates do not produce positive earnings.

One should quickly realize that because the Federal Reserve Bank pays a positive 50 basis points on cash reserves, banks across the G-20 would prefer to hold excess cash at the US Federal Reserve instead of at their own central banks — and foreign banks can do that by making deposits at the Fed via their US subsidiaries.

Here’s the implication: There is a substantial need and incentive for banks not only in the US but also across the G-20 to hold excess US dollar cash reserve deposits at the US Federal Reserve Bank.

Below is shown total cash reserves at the Fed and its division between required and excess cash amounts, starting just prior to the financial meltdown. The total cash owned by banks rose starting with post-financial crisis QEs. Total cash derives from the Fed buying assets and paying in currency (or claims that can be converted to currency) and that cash, in turn, being deposited by the seller at his or her own bank.

By US banking law, the portion of cash from that transaction that is required is a rather small proportion of the deposit. So in total, the new cash becomes divided between required cash (shown as the narrow strip in brown at the bottom of the graph) and the “excess” of what is required.

The amount of excess cash, shown in blue, is large in absolute and relative terms ($2.37 trillion, presently) as compared to a normal level of zero held for many prior decades. That is, banks were fully loaned up given the cash amounts provided by the Fed and all cash was required.

This condition of excess bank cash has, since Keynes’ time, been characterized as a “liquidity trap.” It was taken as synonymous with depressionary circumstances where borrowers did not wish to borrow and lenders did not wish to lend, causing high proportions of excess cash.

But now, there is a new incentive for banks (and not just US banks) to hold excess US cash. It meets the BIS liquidity requirement while also being paid 50 basis points by the Fed. From the bank’s perspective, that is a decent return on riskless paper that cannot depreciate due to falling bond prices, which typically occurs when they need the cash most — i.e., in a financial meltdown. It’s a reasonable way to meet the LCR requirement.

So if an individual commercial bank needs to meet its LCR, it sells assets and deposits the proceeds with the Fed. It would not be putting the cash into loans and paying for the loan with deposits (the usual commercial bank money expansion method) because the deposit would create the need for the bank to use some of its new cash as required reserves and it would not contribute to its LCR requirement.

This is hardly a prescription for monetary policy to generate lending and spending to achieve the macroeconomic objectives of job growth and inflation.

So now, hopefully you see the irony. Though the Fed has embarked on multiple quantitative easing operations of expanding its balance sheet in order to stimulate commercial bank lending and spending, it’s not happening to the extent it would have formerly occurred.

It is the increased need to hold cash, as dictated by the BIS liquidity requirement, that causes banks to hold excess cash rather than lend it out. This is what is creating the liquidity trap. And it’s not just true for US banks: Cumberland Advisors estimates that 44% of the excess US bank cash held at the Fed is in accounts belonging to US subsidiaries of foreign banks.

It used to be that the money supply multiplier concept gave testimony to the importance and strength of monetary policy. It had been the case that when the central bank printed money and bought assets, credit availability would get a boost from these central bank purchases, but the far greater boost came from commercial banks’ subsequent expansion of loans. This has been called the money supply multiplier because banks expanded credit in amounts 8 to 9 times the Fed’s increase in its asset purchase.

That is quite a money supply multiplier.

This multiplier gave the Fed and its monetary policy an extraordinary influence on credit availability and a much greater impact on the economy than it would have had through its own direct purchase of assets.

Thus, in today’s discussion of why the Fed’s expansionary policy is not reviving the economy, one need look no further than the banks’ muted response to it. The accompanying graph shows the growth of US commercial bank assets since 2008.

The Federal Reserve balance sheet has expanded 500% since the pre-financial crisis times of 2008 via Fed QEs, while the combined bank balance sheets have increased only 45%. Or to put it another way, if the responses of commercial banks to the Fed expansion were in the same proportion as the pre-financial crisis relationship of commercial banks and Fed balance sheets, the combined commercial bank assets today would be $55 trillion vs. its actual level of $l6 trillion.

To understand how under-expanded and under-loaned banks are, realize that half of the commercial bank expansion is not due to additional loans but rather to banks holding the additional cash the Fed spent on assets that then became deposited at the sellers’ bank.

So the Fed’s influence on growing credit and on the economy has largely been stymied by the new required liquidity amounts — all with the goal of averting the next financial crisis. And the press hoopla about what the Fed will do next has become a carnival sideshow that embarrasses the Fed because when it steps on the monetary accelerator, very little happens.

What the Fed needs is a low PR profile for its own good when it comes to its ability to restore full employment and inflation. It creates false expectations that can’t be realized while there is a BIS liquidity requirement that’s neutralizing its expansionary policy.

What we have is a situation in which regulators with different mandates are working at cross purposes with each other, with the BIS forcing cash holdings (and other liquid assets) to prevent illiquidity in a crisis, and the Fed providing cash with the hope that banks lend it and borrowers spends it.

The Fed giveth, and the BIC taketh away.

The bottom line is that the Fed (and other central banks) have supplied cash, but much of it has been hoarded to make sure bank runs and financial crises are a thing of the past. So if the Fed were to provide economic stimulus consistent with its objectives, it needs further expansion rather than the “normalization” of its balance sheet to 2008 levels.

Click to Email Dr. Spellman

Is their loyalty to government subsidization above their responsibility to their own central banks’ balance sheets and the commercial banks they regulate? Or are they fools who have been seduced by Keynesian central bank ideology in which lower interest rates are seen as always better for the economy? And that includes

Is their loyalty to government subsidization above their responsibility to their own central banks’ balance sheets and the commercial banks they regulate? Or are they fools who have been seduced by Keynesian central bank ideology in which lower interest rates are seen as always better for the economy? And that includes

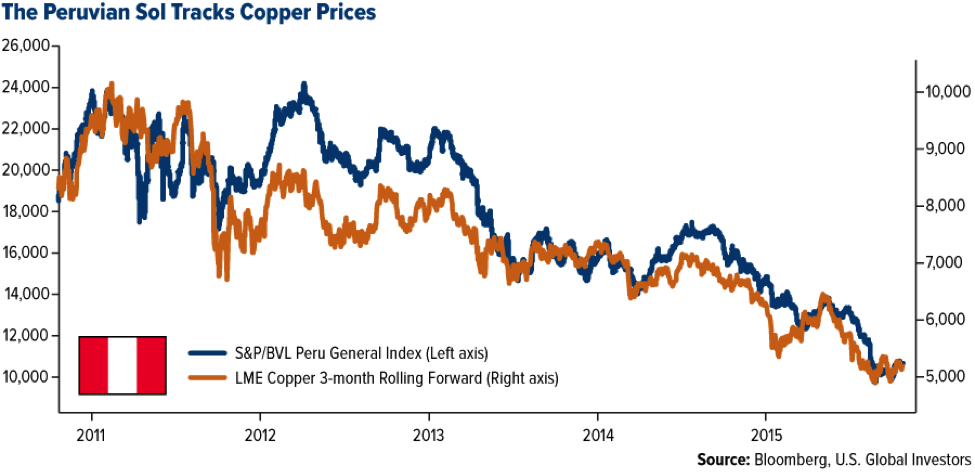

Foreign capital provides jobs and income, but it becomes problematic because it is seldom applied at a steady and measured pace in proportion to the opportunities. During the Great Recession, the Fed’s QE provided investors with a large liquidity pool disproportionate to the onshore investment opportunities, so a good deal of that liquidity gushed into off-shore investment. And much of that went to the commodity and energy industries, which, at the time, were supply-constrained and expensive. These include Brazil, Indonesia, Russia, South Africa, and Chile, Peru among others, as well as some developed country plays in Australia, West Texas, and Canada. In investment booms fed by outside (and not very discerning) capital, animal spirit-driven developers keep on borrowing and building to be absorbed by the market before their competitors, and the unrestrained booms that follow result in over-building, excess production, inventory build-ups and in turn soft prices, debt defaults, eventual bankruptcies, and penny stocks. That much is true for any domestic boom and bust, but now there is a foreign twist when the projects are debt-financed from offshore sources that typically require repayment in US dollars. Hence, foreign-financed investment has a built-in currency crisis in the making when settlement takes place because it drives the price of the US dollar upward and the local currency downward. Predictably, it comes at a time when the boom is over-built, leaving investors scrambling to generate revenue, and commodities continue to be sold at very low prices in order to cover the rising cost of dollar-debt repayment. There is a rush to extinguish dollar debt before a property is lost to foreclosure, which, in turn, leads to major multiple market reactions – all downward. The selling of commodities at ultra-low prices creates an adverse currency movement for the affected country. For example, see the correlation (below) of the declining price of copper relative to Peru’s Sol and Iron Ore relative to the Australian Dollar.

Foreign capital provides jobs and income, but it becomes problematic because it is seldom applied at a steady and measured pace in proportion to the opportunities. During the Great Recession, the Fed’s QE provided investors with a large liquidity pool disproportionate to the onshore investment opportunities, so a good deal of that liquidity gushed into off-shore investment. And much of that went to the commodity and energy industries, which, at the time, were supply-constrained and expensive. These include Brazil, Indonesia, Russia, South Africa, and Chile, Peru among others, as well as some developed country plays in Australia, West Texas, and Canada. In investment booms fed by outside (and not very discerning) capital, animal spirit-driven developers keep on borrowing and building to be absorbed by the market before their competitors, and the unrestrained booms that follow result in over-building, excess production, inventory build-ups and in turn soft prices, debt defaults, eventual bankruptcies, and penny stocks. That much is true for any domestic boom and bust, but now there is a foreign twist when the projects are debt-financed from offshore sources that typically require repayment in US dollars. Hence, foreign-financed investment has a built-in currency crisis in the making when settlement takes place because it drives the price of the US dollar upward and the local currency downward. Predictably, it comes at a time when the boom is over-built, leaving investors scrambling to generate revenue, and commodities continue to be sold at very low prices in order to cover the rising cost of dollar-debt repayment. There is a rush to extinguish dollar debt before a property is lost to foreclosure, which, in turn, leads to major multiple market reactions – all downward. The selling of commodities at ultra-low prices creates an adverse currency movement for the affected country. For example, see the correlation (below) of the declining price of copper relative to Peru’s Sol and Iron Ore relative to the Australian Dollar.

This strong currency decline then causes unrelated companies, individuals, and even governments to sell most anything denominated in local currency and use the proceeds to purchase US dollar-denominated assets. The debt repayment wave deteriorates into a generalized capital flight and a currency collapse for the involved country. Basically, the bright shining buildings shown above are still standing and shinning, but in the economic and financial dimensions, all prices are falling down. This is the basic scenario that followed the early days of globalism in which there was an over-build of manufacturing capability in the cheap labor countries of Asia in the 1990s. The consequence was a bust phase known as the

This strong currency decline then causes unrelated companies, individuals, and even governments to sell most anything denominated in local currency and use the proceeds to purchase US dollar-denominated assets. The debt repayment wave deteriorates into a generalized capital flight and a currency collapse for the involved country. Basically, the bright shining buildings shown above are still standing and shinning, but in the economic and financial dimensions, all prices are falling down. This is the basic scenario that followed the early days of globalism in which there was an over-build of manufacturing capability in the cheap labor countries of Asia in the 1990s. The consequence was a bust phase known as the

and act on the regulatory reports or what is the dollar cost of corporate and personal compliance to regulation? Does that make the argument?

and act on the regulatory reports or what is the dollar cost of corporate and personal compliance to regulation? Does that make the argument?

Some 70 years ago, Congress spelled out the economic growth objectives for the U.S. economy in the Full Employment Act of 1946. The mandate was for the government to support policies that would bring about sufficient economic growth so that employment would become “full.” Congress also included a restraint to the mandate that would limit inflation, but over time, both interpretations and priorities change. After all, this is politics as well as policy.

Some 70 years ago, Congress spelled out the economic growth objectives for the U.S. economy in the Full Employment Act of 1946. The mandate was for the government to support policies that would bring about sufficient economic growth so that employment would become “full.” Congress also included a restraint to the mandate that would limit inflation, but over time, both interpretations and priorities change. After all, this is politics as well as policy.