The Second Coming of the Conundrum

So You Think the Federal Reserve Controls Interest Rates?

The Second Coming of the Conundrum

The mention of globalism causes most people to think of open trade, but globalism has another dimension to it. And that is financial globalism. It can’t be overlooked as it likely has a greater influence on financial markets than the Federal Reserve. Furthermore, it contributes to why the Federal Reserve does not seem to be able to control the long term interest rate, a condition known as the Conundrum. It’s back again.

But first, a little background.

Prior to the World Trade Organization (WTO) coming on the scene in the 1990s, most countries wouldn’t allow their financial resources to flow outward to another country. The thinking was that if their own citizens had saved, governments should restrict those scarce savings to finance production within their own borders. That is to say, if an automobile plant were to be built, governments wanted it be built on their own shores and not in Detroit, as in pre-globalism days. Furthermore, government thinking was that if domestic savings was not channeled to financing home-shore production, it could be directed to purchase home country government bonds that could cover their own fiscal deficits.

Hence, capital outflow barriers were built. Capital had a hard time leaving most countries around the globe, including most developed countries of Europe. The few exceptions were those countries that allowed free entry and exist of capital, both foreign and domestic (a pre-requisite for becoming a reserve currency country, by the way). And when foreign capital was free to both enter and leave, financial sectors emerged that offered deep and diverse investment menus to foreign investors, including the US.

That all changed when the world focused on the mutual benefits that could be derived from open trade, or what we identify today as “globalism.” Globalism was not just about lowering barriers to trade but also reducing barriers to capital flows. What unfolded was a variety of pacts, most prominently the WTO, by which member countries became committed to opening capital outflows — and capital did indeed flow out. This, then, affects the demand and pricing for securities wherever the capital chooses to land.

Higher US securities prices and lower bond yields were the first signs that foreign capital was creating greater demand, as explained in a 2005 analysis by Ben Bernanke, then a Federal Reserve Governor.

What caught Bernanke’s attention was the fact that long-maturity US bonds were appreciating as market yields trended lower at a time when the Fed was attempting to raise interest rates. The Fed was successfully raising short-maturity yields by selling short-dated bonds, but long- maturity bonds yields mysteriously moved downward.

This condition is called a yield curve flattening or inversion, depending how far it goes. For a closed economy, this is typically the result of investors choosing long-maturity bonds when they believe a disinflationary recession is in the offing, and they want to lock in the long-dated yield while it is still available. But this occurred in 2005 while the economy was “performing well” and inflation was “anchored” — in Bernanke’s words — so any thought of an impending US recession and disinflation was fleeting because the economy was entering the housing boom era. Hence, the recessionary explanation of why domestic investors would move into longer maturity debt and drive yields downward did not hold.

In sorting things out, Bernanke turned to the changes in the interest rate environment under globalism. He pointed out that some countries, especially in Asia, benefited from running a large trade surplus. This indicates that a nation earns more foreign currency than it spends in that foreign country. It accumulates a balance of the trading partner’s currency. It is also called a saving surplus, if it is greater than what it spent on domestic investment in plant and equipment. This residual provides a financial surplus that will be invested in financial markets. And with the opening of foreign markets, much of that financial investment gravitated to the US and took the form of long-term bond holdings which drove long maturity yields downward.

This raises the fundamental question of whether the Fed, despite all its pretense of managing and manipulating interest rates, can really do so in the face of open global trade in which foreign countries are running the trade surpluses and open global capital markets allowing the winners in trade to invest it’s surpluses in the US markets.

Shortly after Bernanke’s saving glut explanation of falling long-term interest rates, the then-Fed Chairman Greenspan, testifying before Congress, was asked to explain why the yield curve was inverting (meaning that as the Fed raised short-term rates, long-term rates were falling). His answer in Greenspanese was, “It’s a Conundrum.”

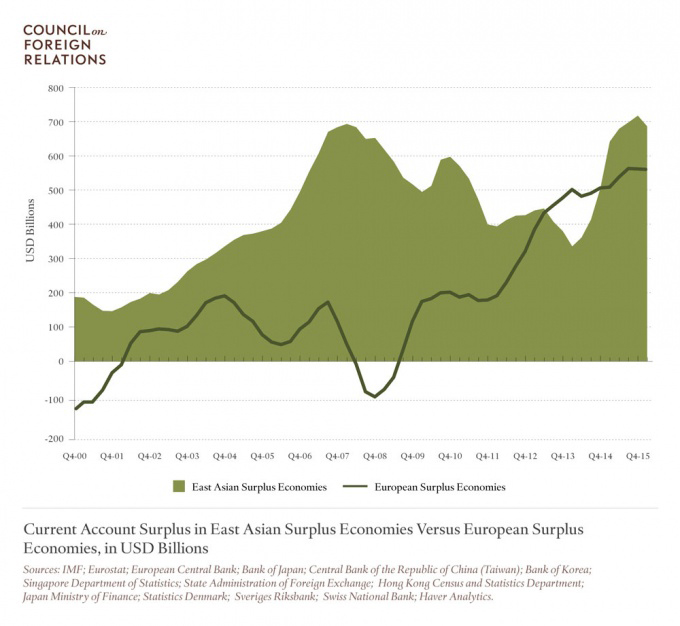

Well, the Conundrum is back today in 2017. The Fed is again seeking to raise rates. It’s been successful with short-term rates by selling short-term instruments, but the long-term rates have been falling since the beginning of the year. What’s also back is another large upswing in global savings in USD, as shown below in data supplied by Brad Setser of the Council on Foreign Relations.

Setser summarizes:

“The combined savings of China, Japan, Korea, Taiwan, and the two city-states of Hong Kong and Singapore is about 40 percent of their collective GDP, a 35-year high. No other region of the world currently contributes more to the global glut in savings that has brought interest rates around the world down to record lows. Asia’s current account surplus — its excess of savings over investment — has increased significantly in the past two years and is now about as large, relative to the GDP of its trading partners, as it was prior to the global financial crisis.”

Note that on the graph the excess savings over investment data is measured in billions of US dollars for both the East Asian and European (Saving) Surplus Economies. Now compare that to the Fed’s selling in their effort to raise rates. It has sold approximately $200 billion of short-term Reverse Repo debt, whereas the surplus savings of East Asia and Europe (depicted above) total approximately $1.2 trillion at an annual rate which is looking for a home in global financial markets. Not much of it has to trickle into the US bond market to offset the Fed’s selling.

So there you have it. If what is lost in trade trickles back into the financial markets, the Fed has lost its power to control market prices and interest rates as they wish. The power to offset the Fed exists and so the US central bank does not control interest rates in the US as it once did in a non-globalism world. And if it can’t, it’s lost its controlling influence over the US economy.