Some 70 years ago, Congress spelled out the economic growth objectives for the U.S. economy in the Full Employment Act of 1946. The mandate was for the government to support policies that would bring about sufficient economic growth so that employment would become “full.” Congress also included a restraint to the mandate that would limit inflation, but over time, both interpretations and priorities change. After all, this is politics as well as policy.

Some 70 years ago, Congress spelled out the economic growth objectives for the U.S. economy in the Full Employment Act of 1946. The mandate was for the government to support policies that would bring about sufficient economic growth so that employment would become “full.” Congress also included a restraint to the mandate that would limit inflation, but over time, both interpretations and priorities change. After all, this is politics as well as policy.

In aiming for full employment while controlling for inflation, the greatest responsibility fell on the shoulders of the Federal Reserve, which had the short-term flexibility to vary the cost of credit to manipulate aggregate demand.

To do so, there had to be an understanding of how much aggregate spending was needed to generate employment levels considered to be “full” without accelerating the inflation rate. This led to the development of a macroeconomic target called “Potential GDP,” which defined how much GDP spending would be needed to create enough demand in markets that would cause firms to hire just the number of workers consistent with full employment. Too few, and targets wouldn’t be met. Too many, and there would be inflation.

The goal, then, was for the Fed to match an equal amount of demand to Potential. This concept and its calculation was the work of Arthur Okun in l962 that become known as Okun’s Law.

The second link of what needed to be established is how that amount of aggregate demand would relate to the Federal Reserve’s main policy instrument, the short-term interest rate. This was accomplished by the Taylor Rule in the early l990s. It provided an estimate of the short-term interest rate that would generate the demand that would cause business firms to hire enough workers so as to be at full employment.

All these machinations of determining the right short-term interest rate to drive spending to the right number that would, in turn, cause businesses to hire the right number of workers to claim that employment is full is an ongoing exercise because the relationships that determine that interest rate are constantly changing. That is to say, the latest calculation of Okun’s Law (how much spending is needed) and the Taylor Rule (what interest rate creates that amount of spending) are subject to the latest economy-wide responses — and those do change.

For Wall Street, the Federal Reserve’s plan to raise interest rates, is seen as an attempt to put a dent in the economy and, hence, corporate profit growth and — in turn — stock prices. What Wall Street doesn’t realize is that the interest rate adjustment is supposedly one that will get the economy to full employment (and prevent inflation acceleration) and keep it there.

But the stock market’s obsession with the Fed’s intention to raise interest rates is largely misplaced: The Fed is looking to maintain growth, while allowing for some inflation which is viewed as a means to depreciate debt outstanding. To the extent there will be an interest rate increase, it’s likely to be little and late and an almost symbolic fulfillment of their duel Congressional mandate.

Nonetheless, all the major stock market indexes for U.S. equities since the beginning of the year are flat, reflecting a deterrent to growth that the Fed rate adjustment would supposedly create.

But there is other reason for Wall Street to be concerned with the general advance of stock prices.

When employment growth occurs, as it has, in this slow-motion up-cycle, labor becomes relatively scarce and wages increase. That’s the whole point of the macroeconomic exercise of targeting full employment. But in turn, rising wage rates increase the costs of production, which reduces profit margins and total profit.

We are at that point for many firms. Actually, we are beyond that point.

The more ominous rate for Wall Street should be the wage rate — not the interest rate — that flows into corporate employee costs. This creates a larger dent to overall profit than is being added either by more output and/or higher prices as the economy approaches Potential.

The wage component of employee costs is now bumping along at close to a 3 percent rate, but that only partially reveals the deterioration of profit due to employee compensation. There is a rarely viewed government statistic called the ECEC, or the Employer Cost of Employee Compensation. This calculates the employment cost to employers, taking into account not only wages but also benefits. Those have amounted to a 4.9 percent increase over the past two quarters.

The employee cost component is rising, but employee benefits are rising at a more substantial pace as the Affordable Care Act (among others) kicks in.

But that still doesn’t fully reveal the dent in corporate profit that will be delivered from tighter labor market conditions. It’s not just employee expenses that matter but also the extent to which those costs are offset by greater productivity of labor. That is, if labor costs rise and are offset by more output per employee, labor cost per unit of output can actually decline, resulting in a larger bottom line. But that’s not happening. Rather, the opposite is occurring.

The Bureau of Labor Statistics indicates: “Productivity decreased 3.1 percent in the nonfarm business sector in the first quarter of 2015; unit labor costs increased 6.7 percent (seasonally adjusted annual rates).” In manufacturing, productivity decreased 1.0 percent and unit labor costs increased 3.4 percent.

The significance of this 6.7 percent increase in unit labor cost must be compared to profit margins per unit. On average, pre-tax profit (as a percentage of corporate value added, as a proxy for profit margins) is at a very high 12 percent per unit produced, as can be seen below. Hence, we are looking at a collection of firms potentially losing half of pre-tax operating profit to employee compensation — and stock market shocks will follow.

Thus there is a built-in contradiction of achieving macroeconomic success of driving the economy to where employment is full and simultaneously providing stock market returns. The only way the two can simultaneously occur is if firms invest in capital equipment to raise productivity more than the growth in employment costs. But that happy state of affairs is not occurring.

So at this juncture of the business cycle expansion, we are looking at increasing labor cost per unit produced with a large dent to profit margins and reduced profits for firms with heavy dependence on U.S. labor. This implies U.S. service industries are the most vulnerable.

But yet there is still a stock market opportunity with widening profit margins for firms that use foreign labor (via outsourcing) and are paid in cheaper foreign currency given the stronger U.S. dollar.

Some firms will benefit from global access to cheaper employee costs. Basically, there will be a dispersion of positive and negative shocks from firm to firm with the ratio of the advancing-to-declining stock decreasing. Some stocks will become dogs and other will be purring cats of profit expansion due to cheap foreign labor.

The implication for investing in a broadly diversified range of firms would mix the dogs with the cats and the outcome would reflect the same: stagnant returns on average, along with a general sense of uncertainty as some firms experience earnings surprises, both positive and negative.

Firms that benefit from this macroeconomic environment are those that deliver goods to U.S. consumers that are produced more cheaply abroad. Detecting and targeting those cats from the dogs in this environment is more the issue for U.S. stock market investors than a generalized fear of interest rate liftoff.

Sign up to receive the Spellman Report. Bracing financial and economic insight. Now with free delivery!

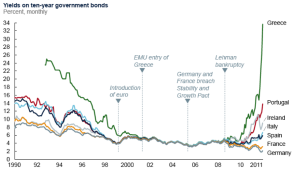

Economic growth in the developed world is falling well short of the post-WWII experience, and there are identifiable causes.

Economic growth in the developed world is falling well short of the post-WWII experience, and there are identifiable causes.

It’s long been in the DNA of economists and market observers, going back at least to the Austrian School of Economics, that when

It’s long been in the DNA of economists and market observers, going back at least to the Austrian School of Economics, that when  money growth outpaces the economy’s growth, booms are created and so are busts: Boombustology, as coined by Mansharamani of Yale University.

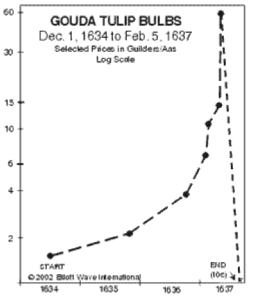

money growth outpaces the economy’s growth, booms are created and so are busts: Boombustology, as coined by Mansharamani of Yale University. That is, the durability of the over built real capital determines the duration of following depressed demand and soft prices. And this condition continues and defines the duration of the bust as long as the excess supplies are a silhouette on the horizon as shown to the right.

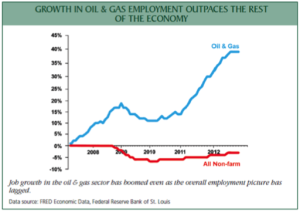

That is, the durability of the over built real capital determines the duration of following depressed demand and soft prices. And this condition continues and defines the duration of the bust as long as the excess supplies are a silhouette on the horizon as shown to the right. extraction have been highly instrumental to the U.S. cyclical recovery.

extraction have been highly instrumental to the U.S. cyclical recovery. and $786 billion in lower rated bonds financing this capital intensive undertaking.

and $786 billion in lower rated bonds financing this capital intensive undertaking.

Officials from the Federal Reserve have agreed that their quantum asset purchases, financed with new money through a process known as

Officials from the Federal Reserve have agreed that their quantum asset purchases, financed with new money through a process known as

At the conclusion of World War II, there was a meeting among the Allies in Bretton Woods, New Hampshire. There, it was agreed that institutional arrangements would enhance the U.S. dollar for across-country payments (as opposed to gold or another currency, such as the British Pound).

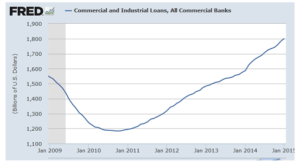

At the conclusion of World War II, there was a meeting among the Allies in Bretton Woods, New Hampshire. There, it was agreed that institutional arrangements would enhance the U.S. dollar for across-country payments (as opposed to gold or another currency, such as the British Pound). In the financial bust of just five to six short years ago, prices of financial assets across the board were in free-fall. Even when prices stabilized at bargain levels, liquid and solvent buyers were frozen in place, unable to bid.

In the financial bust of just five to six short years ago, prices of financial assets across the board were in free-fall. Even when prices stabilized at bargain levels, liquid and solvent buyers were frozen in place, unable to bid.