Officials from the Federal Reserve have agreed that their quantum asset purchases, financed with new money through a process known as Quantitative Ease (QE), will conclude next month — that is, unless they find a new problem on the horizon for which another dose of quantum money seems in order.

Officials from the Federal Reserve have agreed that their quantum asset purchases, financed with new money through a process known as Quantitative Ease (QE), will conclude next month — that is, unless they find a new problem on the horizon for which another dose of quantum money seems in order.

And lest we presume that we have lived through the conclusion of this epic historical monetary experiment, we now find the European Central Bank [ECB] has re-ignited. And ditto for the Bank of Japan, as things are not going well in either location.

And just like the Fed — in an effort to take Keynesianism not just to the limit, but beyond the limit of credulity — the ECB has set a negative nominal rate target.

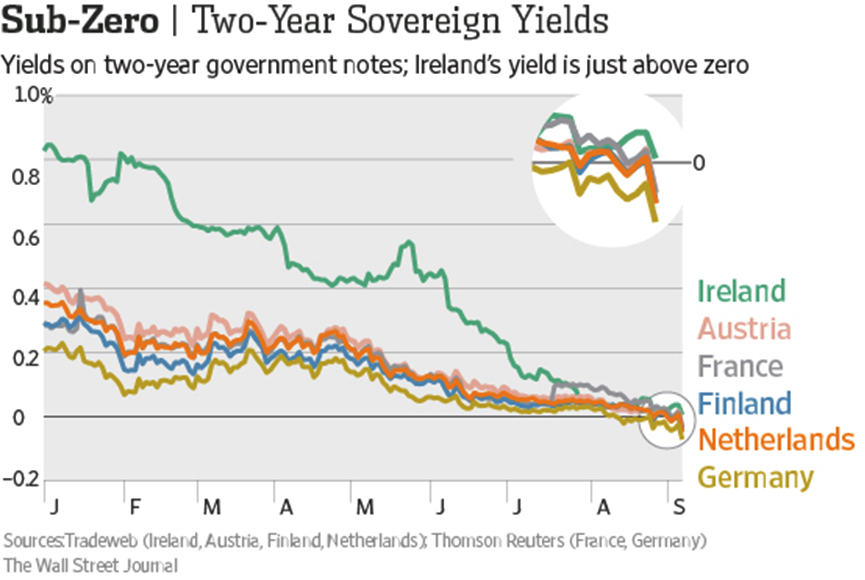

Now, it’s one thing to set a service fee on deposits that exceeds any interest paid to achieve a negative rate. But if you can image it possible, market yields of traded European sovereign bonds have actually turned negative for possibly the first time in human experience, as shown below:

This is achieved when an investor voluntarily pays a price for a debt instrument that is higher than the investor will receive back in both principle and interest. And mind you, this is by contract, not by default.

Not since the days when Mark Twain’s Tom Sawyer charged his friends for the privilege of painting his fence has the world gone quite so upside down and backwards.

And upside down and backwards it is when central bankers, in their zeal to entice borrowers to borrow in the hope that they will spend and generate income, have now pushed interest rates not to zero but actually into negative territory. This amounts to the subsidization of borrowers (whether they are consumers, businesses, or governments) saying: “Please, take the money and spend it, and you don’t have to pay it all back.”

So the question is, why would central banks do this? Well let’s examine the rationality in Fed Chairwoman Yellen’s own words:

“The Fed provides this help by influencing interest rates. Although we work through financial markets, our goal is to help Main Street, not Wall Street. By keeping interest rates low, we are trying to make homes more affordable and revive the housing market. We are trying to make it cheaper for businesses to build, expand, and hire. We are trying to lower the costs of buying a car that can carry a worker to a new job and kids to school, and our policies are also spurring the revival of the auto industry. We are trying to help families afford things they need so that greater spending can drive job creation and even more spending, thereby strengthening the recovery.

When the Federal Reserve’s policies are effective, they improve the welfare of everyone who benefits from a stronger economy, most of all those who have been hit hardest by the recession and the slow recovery.”

Well I beg to differ with you, Madame Chairwoman, on your narrow-minded concept of the “welfare of everyone.”

Who, other than central banks, has the luxury of being more or less indifferent as an investor in zero (let alone negative-yielding) market debt? The trillions spent to put the relatively small group of now-reluctant workers with challenged skills to work inflict serious economic pain on the other side of the coin, so to speak.

And on the other side of the cheap money coin is the absence of investment income of a large generation of savers and future retirees called Baby Boomers (amounting to 30 percent of the U.S. population), as well as their supporting institutions such as pension funds, insurance companies, and endowments that provide medical and educational benefits.

Zero interest rates do not come anywhere near the assumed earnings rate of individuals or institutions to service future retirement or endowment obligations.

But normalizing to higher interest rates generates another larger problem than the immediate problem of a semi-lackadaisical economy.

And that problem is that a subsequent shift to normalized higher interest rates (to create investment income for institutions and individuals for retirement purposes) causes the enabled borrowers in the ultra-cheap money scheme to face rising costs of repayment, which in turn requires them to reduce their spending.

This is the conclusion of the Bank of England with regard to central bank encouraged household debt and the fiscal austerity in Europe and the implementation of a national sales tax in Japan is a de facto recognition that previous borrowing binges at cheap interest rates compromises the economic future.

This demonstrates that Keynesian notions of debt-enabled spending policies have maxed-out, as there is too much accumulated debt, and the process has become counterproductive. For the U.S., we have a bit more running room until we hit the wall, but in the decades ahead, Baby Boomers will suffer the consequences of previous central bank myopia.

Ultra low interest rate enticements to spend create multiple future problems. Those with the debt subsequently seek to deleverage especially when interest rates normalize thus creating future recessions. Then in an effort to prevent those future recessions, the central bank returns to yet, lower interest rates for a longer period of time thus compromising the calculations and welfare of savers. This is the story of Japan and now Europe. They’ve returned to the money well as the Fed itself has done three times since the onset of the Great Recession

When will the Fed’s monetary zealots understand that future recessions and diminished investment income is not in the “welfare of everyone?”

Debt-generating demand policies were not meant to be a long-term, ceaseless debt accumulation but rather a short-term, cyclical shoring-up of an economy to allow for debt retirement in an ensuing period of prosperity.

At this point, all that is left is supply-side policy, and in that there are rich dividends. Countries will seek out a Plan B, as discussed here that nurtures companies and commerce with a minimum of regulation and taxation to foster economic growth. Keynesian, demand-side policies have been taken to their logical, counterproductive conclusion and the Chairwoman’s sense of “the welfare of everyone” is in the best interest of no one.

Sign up to receive the Spellman Report. Bracing financial and economic insight. Now with free delivery!