At the Cross Roads of Money and Inflation

We all have in our heads the instinctive notion that more money circulating in an economy is inflationary. Indeed the notion of the proportionality of money and prices exists in academia as well. It is known as the quantity theory of money, for which Milton Friedman received a Nobel Prize in 1976.

The proportionality of money and prices has a long history. It probably first derived from events when gold was the money in question: when more of it was found on the ground, it directly resulted in more money jingling in pockets, which led to more spending and, ultimately, inflation. Indeed, the notion of inflation being tied to money has carried over to when central banks took charge of their countries’ money supplies. Since they don’t sprinkle it on the ground, the route from new money to inflation is quite different.

In the US, we recently lived through an episode in which the central bank increased outstanding Federal Reserve Notes 444% between 2008 and 2014 (from $800 billion to $4.5 trillion) while over the same time, the Consumer Price Index rose less than 20%. This is hardly proportionality in the increase of money and prices.

This enormous deviation of facts from theory cries out for an explanation, especially now that an unprecedented event is bringing proportionality back into focus: the central bank is undertaking a planned reduction in money. Are we to expect deflation in a proportionate ratio?

Looking at the special circumstances of the last decade, the housing/mortgage bust caused the Federal Reserve to launch a heroic effort to save the world from a reoccurrence of a banking meltdown à la the Great Depression. Given those fears, the Fed thought it appropriate to support asset prices, especially the kind that were owned by banks. Hence, the central bank purchased large quantities of US Treasuries and mortgage securities.

But the Treasury bonds that the Fed purchased were previously issued Treasury securities that had been purchased from private holders, typically financial institutions. The acquisition of the US Treasury securities by the central bank from third parties was done according to law so as to avoid the appearance that the central bank was monetizing government expenditures.

The distinction of purchasing Treasuries from existing private holders as opposed to purchasing from the Treasury is important to understanding what followed.

As the Fed acquired US Treasuries from private owners and paid for them with its own currency, this set the investment management world into a scramble to find and purchase substitute assets for the Treasury bonds that were just sold to the Fed (in return for Fed cash).

In the world of asset management — whether it be by commercial banks, pension funds, insurance companies, or endowment funds — there is a relatively short list of substitute assets that investment managers are allowed to hold in the institution’s portfolio that conform with the obligations of the institution. Dollar-denominated high-quality corporate debt is likely next on the list for most institutions, but some allowance usually is made for some amount of dividend-paying common and preferred stock, REITs, foreign sovereigns, or other high-quality debt.

While managers have lists of approved assets to purchase and hold, they will ultimately need to branch out from US Treasuries. This is because as the Fed buys Treasuries, it raises prices and lowers yields to the extent that institutions would likely not meet their minimum investment income by buying more of them.

So the purpose of getting money into circulation was essentially for the central bank to spend the money on institutional assets. The Fed had hoped that its actions would help fight the ongoing recession by allowing more investors to sell their assets at capital gains and possibly spend some of the proceeds in consumer or business goods markets. If that were to happen, it would be called a “wealth effect” on spending, but it did not occur in a measurable amount, much to the Fed’s disappointment.

All that this new money did was create inflation in asset prices in the financial markets, which did not bleed over into demand for consumer goods as newly discovered gold once did.

Part of the reason the new money did not move the consumer spending dial, and hence inflation, had to do with the condition of the banking system at the time. It had been typically true that when the central bank purchased US Treasuries with fresh currency, it would create fresh cash inflows to banks, providing them with the liquidity to increase lending to other spending units — not just dollar for dollar, but with a large multiplier.

The Fed’s massive asset buying spree generated gargantuan amounts of cash inflows to banks, which did not translate into as much lending as anticipated. The good old banking multiplier had been 8 times the central bank’s original currency injection into the banking system, but during the Great Recession, the bank lending multiplier dwindled to a mere 2 times.

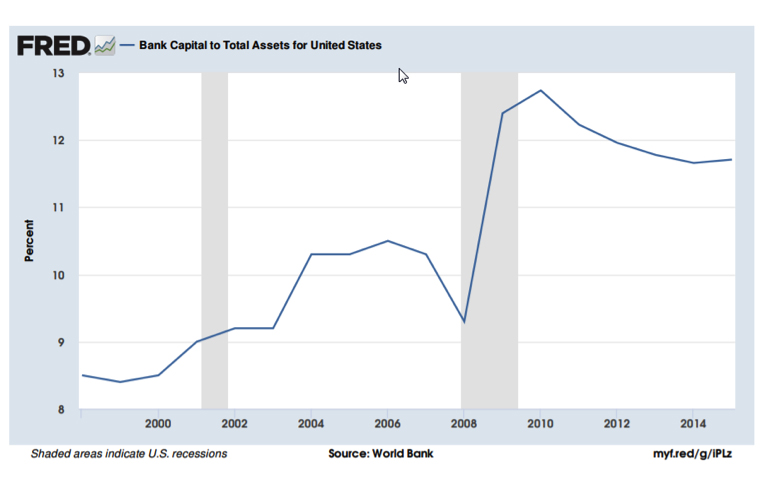

This muted lending response by commercial banks no doubt had to do with another Great Recession peculiarity. During the financial meltdown, as market asset prices dropped, the value of bank assets had to be written down, as per the accounting rules at the time. These rules also required banks to write off their capital (net worth). So despite the great cash inflow, institutions were generally facing depleted capital relative to assets and did not have the necessary net worth or capital ratios required to expand their balance sheets.

So there you have it. The banks’ capital scarcity de-coupled the linkages between new central bank money, additional goods market spending, and inflation. No matter how much cash banks had, they couldn’t lend it without the regulator-imposed safety net of more capital.

But now years later, the bank capital ratio has grown relative to assets (as shown in the graph above), so banks are actually in compliance with new higher regulatory capital ratios than those that existed before the financial crisis. As a result, the common-sense notion of the linkage of money to inflation is again likely to be relevant, as banks can again adjust their balance sheets when they possess excess cash reserves. But since the Federal Reserve is sticking to its 2% inflation target, it’s highly unlikely they would push the contraction of money to the point of generating deflation.