The Anniversary Blues

Economic cycles have been around for a long time, and the National Bureau of Economic Research keeps score, so to speak. US cyclical expansions since 1900 have averaged just short of 5 years in length. The shortest had a duration of but one year, in contrast to our current expansion, which began in the Great Recession low of nearly 10 years ago. If the economy continues to grow through next spring, this would become the longest expansion since the NBER began counting 118 years ago. Meanwhile, the stock market has been ascending for virtually the same amount of time. This is unsurprising, as the two are closely related.

The extended growth of the economy and the stock market now has some investors unnerved, particularly approaching milestones such as the tenth anniversary of the Lehman Brothers implosion. Whenever such an anniversary comes around, a cottage industry of analysts predicts the next bust on the presumption that somehow time is up. After all, analysts need to sound alarms to maintain their respectability in case one were to occur. In the forecasting game, bragging rights are earned by sounding the alarm ahead of a recession; false alarms are tolerated and even considered preferable to totally missing the next downturn.

So where do we stand today? Are we on the edge of another correction, or is more growth on the horizon?

First, some background on the boom/bust process. Relatively fast economic expansions require spending on a particular type of good (or goods) to accelerate at rates above the long-term average. The increased spending on the “boom item” in turn generates additional income for those who produced and sold those items. These producers and sellers then spend their newfound income on other types of goods in the market, creating a multiplier effect that can fuel an extended recovery.

Furthermore, the acceleration of spending in excess of income tends to lead to borrowing, so economic expansions come along with credit expansions. When the economic expansion ends, the debt that financed the expansion now accelerates the ensuing recession as more income becomes devoted to debt reduction.

The economic expansion proceeds until excess demand for the boom items gives way to an excess supply of it. When the borrowing and spending stops, income growth lags and defaults start to pile up. Therefore, the first cousin to economic distress is financial distress, most typically with bank lenders.

Additionally, stock market retreats become a second cousin to the slowdown in economic growth. When the market dips, fewer boom and secondary items are sold, and they sell at lower prices and smaller profit margins.

That is the general outline of the business cycle, accompanied by a lending cycle and a stock price cycle.

As an example, the tech boom of the 1990s was driven by spending on personal computers and software. When the market became satiated, sales slowed, and the ensuing tech bust led to monetary policy that generated easy money to support spending. The main beneficiaries of this policy became the housing industry, as consumers borrowed the cheap money and spent it primarily on new or existing houses. That became the boom item that propelled the next economic expansion — until that market also reached satiation.

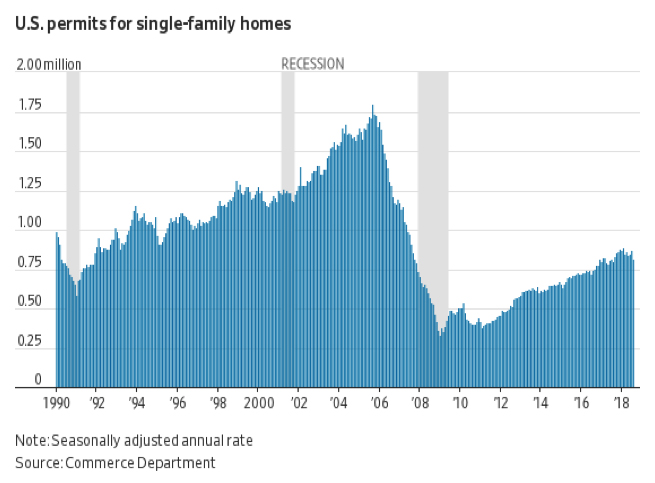

The chart below shows housing permits by year relative to recessions, which are shown in a gray shade. You can see that housing really got into expansionary mode on its way to becoming the next boom item after the 2000 tech bust. The housing market extended itself until it was overdone, and it actually began to decline before the full-fledged bust of 2007-08, with new housing permits falling from a peak of 1.75 million to approximately 350,000 per year.

Faced with another recession, the Fed this time put the pedal to the metal with its Quantitative Ease, which drove interest rates down to the absolute lowest borrowing rates in history. In the wake of the real estate bust, the chances of a successful housing-driven recovery were destined to be slim. Indeed, in the recovery that followed, annual GDP growth struggled at the 1% rate and the recent eduction in housing starts indicates it was running out of steam in the last year.

If the present economic expansion was dependent on easy money to continue the expansion based on consumer durable goods, then I would have to agree with the naysayers with the anniversary blues and are predicting the next recession.

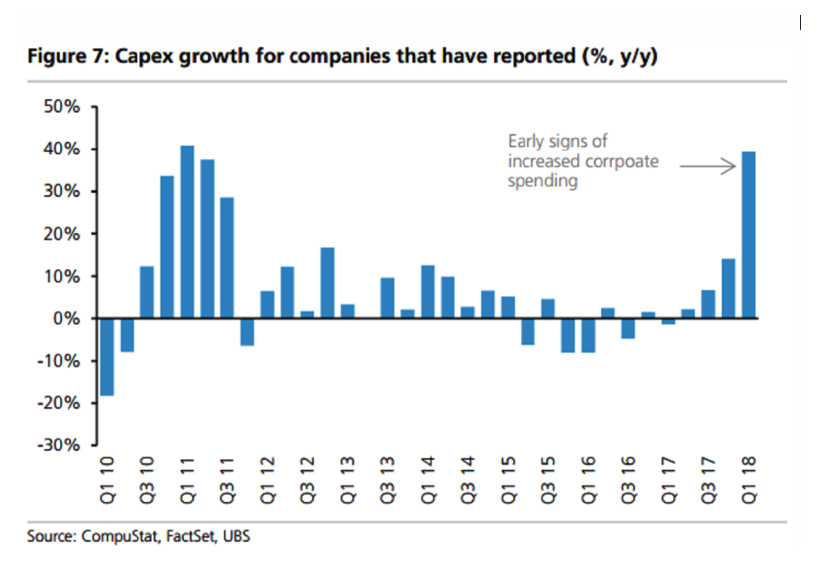

However, has life sprung back into the economy more fundamentally in the last year, almost out of nowhere from a different source. This time, rather than housing, the boom item came in the form of invention leading to business capital spending known as Capex.

The “animal spirits” propelling today’s business sector growth are derived from a significant reduction in corporate taxes, accelerated depreciation, the low tax rate applied to the repatriation of foreign earnings and the removal of regulatory constraints. The combined effect of these factors has put the economy into an old-fashioned business investment boom.

Businesses have responded to these incentives by investing in promising new technologies based on artificial intelligence, robots, machine learning, and semiconductors along with new product development in biotech. These new boom items are driving the economy and stock market forward.

In addition to ramping up the demand side of GDP, business capital spending also has healthy supply side contributions. It positively affects productivity, which reduces costs, widens profit margins, affords higher wages with workforce expansion, and acts as a deterrent to inflation. This is a very different expansion as compared to a monetary policy driven debt financed consumer durables spending binge.

This climate of innovation and technological development is creating new leaders in the stock market while also creating losers as markets evolve to new products and suppliers. Market indices are rising but with large differences in the pricing and potential of the disruptors and the disrupted. Stay on your toes, as some brand names will be replaced and disappear.

If the expansion reaches a record length in 2019, that will be an anniversary worth celebrating and the momentum should carry us as long as profit is being generated from break through products and processes as it is doing now.