The Trump Tariff Offensive

Tariffs revision designed to cure trade deficits have become a live and contentious economic policy issue.

Despite the ripples it creates, confronting the trade deficit is long overdue given its importance to such things as reducing the economy’s growth rate, and all that follows in terms of jobs, wages and income.

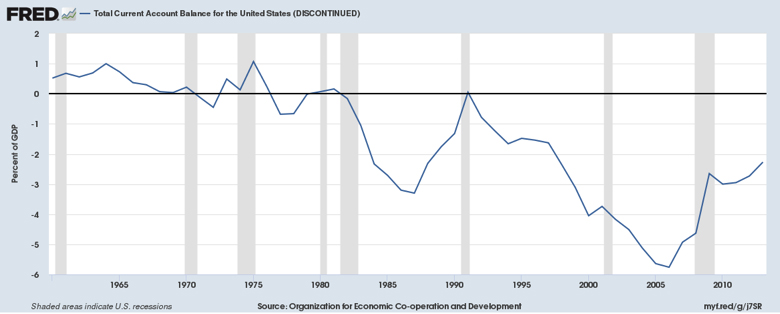

For a long time in the post WWII era, the US trade balance with the rest of the world as a percent of GDP was a small positive number, that is, we had a trade surplus as shown below up until the early l980s. Thereafter, US trade balance swung to deficits in the territory of -3% of GDP in most all years. Most eye catching was a year in which the trade deficit reached -6% of GDP. It is a wonder that in the face of these spending leakages from the US income stream that the economy was able to grow at all.

However, railing at the trade deficit and the loss of US income when income is spent for foreign made goods is a bit short sighted, as this is hardly the full picture of the economic de-habilitation that occurs.

Consider this: When foreigners succeed in running a trade surplus with the US, they accumulate US dollars and if they are greater than their investment needs in plant and equipment, those excess dollar balances are looking for a home in US assets. This is their current account surplus

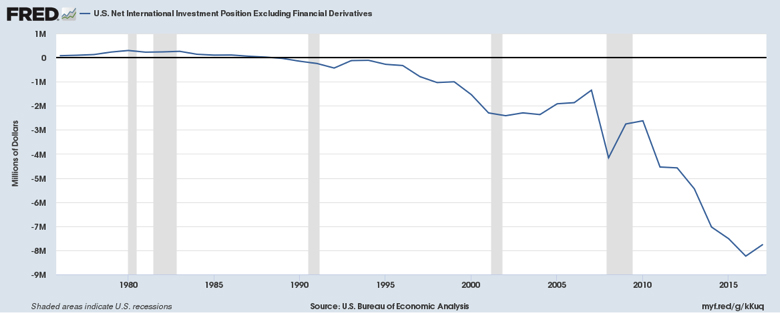

For decades when the US typically ran small positive trade surpluses, successful US exporters were able to accumulate foreign assets and the opposite happens when US trade surpluses turned into trade deficits. In the foreign asset accumulation game what matters is the net holdings of each other’s assets. This goes by the name of the US Net International Investment Position that has become negative as shown below since US trade deficits began accumulating starting in the early l980s.

The three plus decades of negative trade performance has allowed foreigner official accounts to accumulate over $8 Trillion of US assets in excessive of US ownership of foreign assets.

Most of those dollars earned by exporters are sold to their central bank in exchange for local currency and the foreign central bank in turn tends to invest those dollars into US Treasury bonds that become the country’s international reserves.

The US Treasury estimates that nearly $6.285 trillion of our approximately $21 trillion debt is now owned by foreign official sources (governments or their central banks). So the other side of the US trade deficit “coin” is the accumulation of foreign official ownership of US Treasuries.

So in the Trump round of tariff negotiations underway, as the US pushes for lowering tariffs against US products, foreign tariff negotiators are no doubt reminding their US counter-parts, that they are providing cheap financing of US fiscal deficits as a quid pro quo to their trade surpluses. Moreover, in these days of annual trillion dollar US fiscal deficits, this foreign official buying of Treasuries matters.

While covering US fiscal deficits with low applicable interest rates is helpful, the depression of US GDP and associated weaker labor markets matters more. Furthermore, it has gone on long enough that the foreign accumulation of US Treasuries at this point should be seen as a vulnerability on at least two counts.

First, these amounts of US Treasuries held by foreign governments are in aggregate approximately double the Federal Reserve’s accumulation of Treasuries. Hence, foreign central bank owners of US Treasuries have the power to sell Treasuries on a large enough scale to depress US debt prices and raise interest rates in US debt markets.

Such recessionary vulnerability would place the Fed on the spot to purchase these disgorged amounts. Dumping US debt in retaliation to the US tariff war or for other perceived disagreements is not hypothetical and it wouldn’t be the first time as there is evidence that it does occur in amounts that have to influence Federal Reserve policy and actions. (See for example, Foreign governments are dumping us treasuries: a chart).

However, aside from these vulnerabilities in controlling US debt market pricing there is the more important issue of the transfer of US income to foreign sources.This occurs when US taxpayer revenues fund the payments to foreign official sources as owners of US Treasury debt.

So seemingly benign trade deficits if in place over the long term ultimately create, in effect, an annuity to foreign government winners of the trade surplus game at the expense of US taxpayers. These sums are now running at the approximate rate of .75 of one percent of GDP per year in addition to the 2.5% GDP loss in the GDP flow rate due to this year’s trade deficit.

So in summary, trade deficits that accumulate over decades matter a great deal to the bleeding of US income. There is not just the “benign” few percentage points of income stream lost each year because of the trade deficits but there is also the on-going cumulative debt service payments extracted from private US taxpayers and paid in large amounts to foreign governments that occur as a result.

So be prepared for bumps and grinds on the tariff-trade front but parity in trade is worth fighting for.