The financial press’s take on the economy and financial markets has lately been cloudy. The growth rate has indeed been drifting and the economy is being subjected to adverse shocks. But let me suggest there is good reason to believe there is a positive direction emerging below the radar of the cross-currents.

The financial press’s take on the economy and financial markets has lately been cloudy. The growth rate has indeed been drifting and the economy is being subjected to adverse shocks. But let me suggest there is good reason to believe there is a positive direction emerging below the radar of the cross-currents.

One way to reveal patterns of growth is to break down or decompose economic time series into long-term secular trends, cycles and shocks, which take on a pattern of random noise. Since the noise sells newspapers, it receives the lion’s share of daily attention, and it can also cloud the economy’s overall sense of direction. Certainly, the recent plethora of shocks — whether tapering and then more tapering, the emerging market sell-off, Obamacare’s attendant ripples, or adverse winter weather — can create a sense of economic drift or even contraction.

But it seems to me that more important cyclical forces are unfolding below the radar, moving the economy so slowly that its movement is barely detectable.

When I say cyclical forces are moving the economy, I mean that they have a life and momentum of their own apart from the shocks and the secular influences. That is, economies slipping downward don’t go to zero, and economies moving upwards don’t go to infinity. Growth sets in constraints — which typically are overinvestment in durables and plant and equipment — indeed leading to an absence of investment in the recession that follows.

Similarly, during times of recession, a backlog of deferred replacement for capital goods occurs and is ultimately fulfilled. This is true whether the capital goods or durables are those of the consumer, business or even the government.

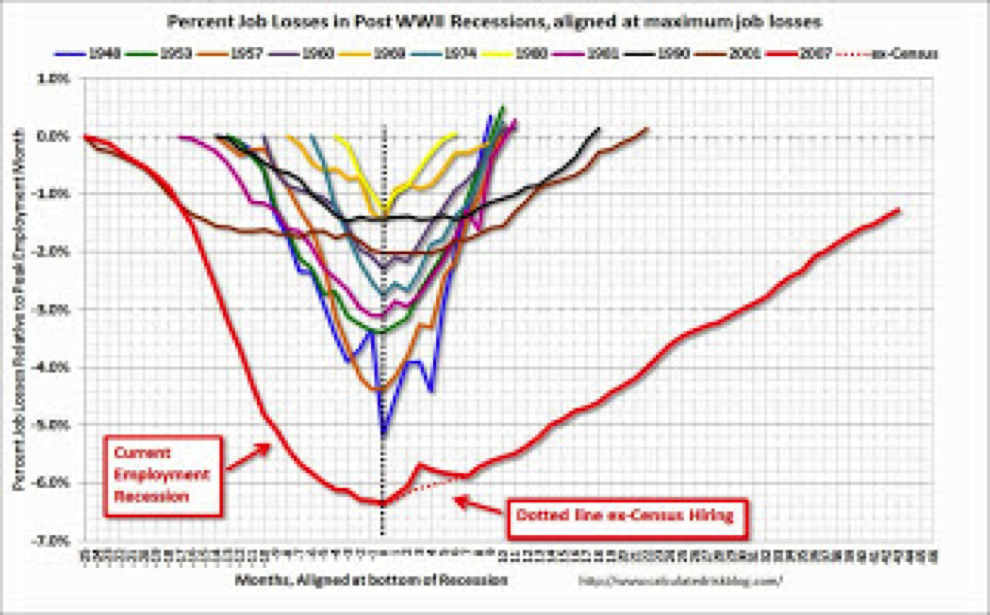

The below graph depicts the duration and amplitude of U.S. employment cycles during the last 70 years or so. The graph reveals that when the economy goes down, so does peak employment from the previous cyclical high. The depiction of cycles is centered on the cyclical employment bottom, which is measured relative to the number of months since the beginning of the recession.

As you can see, most of the post-WWII cycles were relatively short and mild compared to our current episode (shown in red), which is still struggling to return to peak employment six years later. The current recession is a long-bottoming-out saucer that stands out from the much shorter and shallower post-WWII business cycles. The graph shows how the current “recovery” has been slow-moving but nonetheless persistent.

Easier and cheaper money has been the usual driving force that lifts the economy out from a cyclical bottom. In the first wave, it stimulates consumer durable spending, including housing after an absence of durable replacement. This revival has already occurred in the U.S., causing a bottoming out of our current great saucer.

The typical second wave of a cyclical recovery is business investment spending on plant and equipment, which kicks in after demand rises faster than the supply side is expanding. The usual pattern is that business meets higher demand levels first by adding labor, which becomes more expensive as it becomes scarce.

The availability of skilled cheap labor in the U.S. is becoming constrained due not just to rising employment levels but also to an unprecedented drop-out factor in labor participation. Furthermore, much of the globalism movement of the past 30 years (i.e., moving production to countries with large pools of cheap labor) has pretty much run its course.

In that situation, the recessionary lag in business investment spending tends to kick in, driving the next phase of a cyclical expansion.

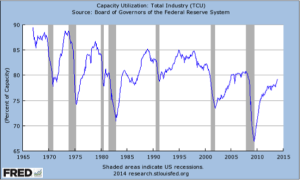

The usual benchmark for this to occur is when industry capacity utilization reaches 80 percent — and U.S. total industry utilization is now knocking on that door at the 79.2 percent level.

Furthermore, most of our emerging market competitors’ utilization rates are above those of the U.S., so the expansion of the capital goods industries is likely to be a global phenomenon.

Furthermore, most of our emerging market competitors’ utilization rates are above those of the U.S., so the expansion of the capital goods industries is likely to be a global phenomenon.

Basically, there has not been a capital expenditure boom since the tech go-go years in the late 1990s, and the capital equipment we do have is aging, with an estimated life of 22 years (up from a more usual 19 years.

Much like my 1999 Pathfinder of the tech year vintage, it has physically worn out, and the usual capital goods replacement phenomenon has me reaching for my wallet. But in that regard the business sector is cash-rich like never before, so the usual obsessing over interest rate elasticity of investment spending is less relevant. If it were relevant, rates are low enough.

Indeed on the financing front, a great deal of financing occurred last year via the non-bank banking sector on top of retaining earnings for years during the recession. To the extent that the Ma and Pa shops did not get in on last year’s financing bonanza, the commercial banking system is showing signs of loosening up credit six years after the shockwaves of 2008, and banks should again become relevant for them.

So basically we are at the point where the baton to keep this race moving forward is in the hands of business cap spending, as consumers are showing signs of constraints in paying for more expensive health care.

The other missing sector that has not been heard from (or at least is not making a lot of noise) is the gradual removal of the net export drag. Available domestic energy is a very positive and long term “shock” to the system.

So cap goods spending, which disappears in recession, reappears at about this juncture of the business cycle, fortified by physical obsolesce, a shortage of skilled labor, and ample cash on hand.

Will this be a typical business cycle recovery? Well, there is nothing about this recovery that is totally classical, as it’s been a classic all to its own. But this fundamental impetus from deferred demand for capital goods stands a high probability of being realized to keep the ball rolling forward.

Moreover, despite governments at all levels attempting to get their fiscal houses in order, there is also a deferred infrastructure demand that will pressure the replacement if not the expansion of the existing roadways across America that are in critical neglect.

While there is good reason to believe that the current cyclical movement will continue into its next phase, one must realize that as employment grows and labor markets become tighter — especially for the skills needed for today’s plant and equipment — labor costs tend to rise as a percentage of the corporate top-line revenue leaves a thinner margin of corporate profits.

So we get into the anomalous territory where growth continues but profit margins and total profit growth decline. So the growth of the economy and the growth of profit diverge at this juncture as an aggregate number, but the focus on the growth industries in this environment makes this a stock-pickers market — unlike last year, when the broad indices outperformed the economy.

As a last note: Cost-push inflation often creeps into this second stage of a cyclical recovery, which causes fixed-income prices to decline in the later portions of cyclical patterns. We should anticipate much the same to happen again, which makes inflation-sensitive income streams more valuable at this juncture.

Sign up to receive the Spellman Report. Bracing financial and economic insight. Now with free delivery!

The dominos are falling. It’s the modern version of a 1930’s bank run. Since everything is bigger (the leverage) and faster (the computers) these days, so is the downfall in financial prices and institutions.

The dominos are falling. It’s the modern version of a 1930’s bank run. Since everything is bigger (the leverage) and faster (the computers) these days, so is the downfall in financial prices and institutions. When these sources no longer provide the liquidity necessary to support the right hand side of bank balance sheets, the bank’s stockholders start to leave in the form of selling bank stock. So the next domino falls. Then stockholders of the banks and other institutions around the world ask their management whether they lent to the hedge funds whose collateralized assets are falling in value. The answer is obviously yes; as we examine the worried look on the face of a very large celebrated hedge fund manager who is pondering what to sell next in order to pay off his leveraged loans and cash out his investors seeking liquidation of their stakes in the Paulson Funds.

When these sources no longer provide the liquidity necessary to support the right hand side of bank balance sheets, the bank’s stockholders start to leave in the form of selling bank stock. So the next domino falls. Then stockholders of the banks and other institutions around the world ask their management whether they lent to the hedge funds whose collateralized assets are falling in value. The answer is obviously yes; as we examine the worried look on the face of a very large celebrated hedge fund manager who is pondering what to sell next in order to pay off his leveraged loans and cash out his investors seeking liquidation of their stakes in the Paulson Funds.

Is their loyalty to government subsidization above their responsibility to their own central banks’ balance sheets and the commercial banks they regulate? Or are they fools who have been seduced by Keynesian central bank ideology in which lower interest rates are seen as always better for the economy? And that includes

Is their loyalty to government subsidization above their responsibility to their own central banks’ balance sheets and the commercial banks they regulate? Or are they fools who have been seduced by Keynesian central bank ideology in which lower interest rates are seen as always better for the economy? And that includes