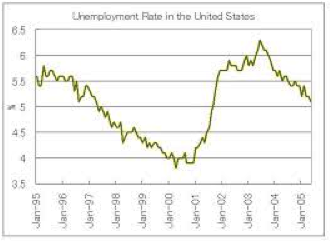

Unemployment narrowly defined is at near 10% or broadly defined is near 17% if it includes those who have quit looking (job search is expensive) and those who are working less than their preferred full time. Also, the length of the economic downturn is approaching two year, which makes this the longest continuous Post WW II downturn.

Simultaneously there are claims that the recession is over. To reconcile these conflicting ideas requires a comparison of actual GDP spending with the GDP that would occur if our resources of labor and industrial capacity were at reasonably full use. This latter concept goes by the name Potential GDP.Potential GDP is a supply side measure of the amount of GDP capable of being produced given available labor and plant and equipment would not add to the inflation rate. While actual GDP could be and is often higher than Potential GDP in economic booms, this implies that the marginal GDP demand is contributing to a higher inflation rate.

In the post WWII business cycles the opposite occurs during recessions when actual GDP spending or demand is less than the GDP that would occur if available resources were employed. In this case the difference is called the deflationary Gap, as this represents soft goods markets. In the current situation actual GDP spending is about 7% less than Potential GDP, which is contributing to an actual deflation. While Actual GDP spending is well below Potential GDP, it has bottomed and has turned around, and it is beginning to grow at a 3% rate. This should be the case given the magnitude of fiscal stimulus and the extraordinary Federal Reserve provision of almost costless liquidity that is reaching certain few entities.

While the actual GDP growth rate has turned the corner from a position far below Potential, this does not necessarily imply that spending will catch up to Potential for several reasons. First, Potential is a moving target that is growing every bit as fast as actual GDP spending is growing at this time if not more. Every month there is an approximate growth of 125,000 new labor force entrants and productivity gains (the flip side of corporate emphasis on efficiency) elevates Potential GDP. In fact the corporate emphasis on cost cutting is allowing more to be built with fewer resources. So GDP spending is chasing the moving target of Potential GDP and is not gaining on it despite the impressions created by the growth chatter. This is in contrast to past recessions when the turn in GDP occurred and tended to catch up to the moving target of Potential GDP within two or three years,implying that GDP spending required growth rates of 5 or 6% during the catch up years.

This leaves the question of whether the “official” recovery from recession by the National Bureau of Economic Research will be proclaimed based on the growth of GDP even if GDP is not in catch up mode and unemployment continues to grow, a situation that might be unique in the Post WW II era. A proclamation by the NBER that the recession is over is based on both qualitative and quantitative issues.

The only thing clear is that if such an assessment is made that it will, in turn, ramp up financial market expectations of rapid growth to full recovery.

DEMAND SIDE HEAD WINDS

The ability of the economy to produce accelerating growth from here to catch up to the moving target of Potential GDP is questionable given the major head winds faced by the economy. This could be a long list but the major items are the following:

The economic growth period of 2003 to 2007 and the economic shock that followed (GDP down at a 6% rate) were not simply a response to rising and falling income as with the typical recession. Rather the growth and decline were a wealth financed economic expansion and contraction. The method for translating consumer wealth into current spending was borrowing, with the majority of the borrowing collateralized by a home. This was called mortgage equity withdrawal. So the economic expansion lead to house building (or refinancing) and debt against said asset. When this ran its course the goods were consumed but we were left with an over-supply of houses that can’t be sold and more debt than could be serviced from income.

This transformation of wealth into spending left a residue of an overhang of approximately 6 million homes (plus commercial real estate) which amounts to a normal three year absorption period though the absorption rate is far from normal. It also left a residue of decline in wealth as the excess houses have deteriorated, housing prices have declined and the mortgage and consumer debt remains unpaid though the consumer is struggling to do so. The extent of the intended consumer deleveraging as seen on page 3 that has taken place is still minor and we remain quite a long way from recovering to theconsumer’s typical debt to income ratios. This effort to service both interest and principle on the debt in turn reduces consumer spending.

Furthermore this wealth liquidation period has left the financial institutions of all varieties and across the globe holding these loans as assets on their books, and the declining values of those loans, in turn,lead to a variety of headline-creating financial meltdowns of institutions as their assets eroded, which in turn eroded their capital after the accounting adjustment was made. These institutions, for the most part, are still barely hanging on and need to shrink their balance sheets to be in proportion to their remaining capital bases. Hence banks are pressing all those who can be pressured to repay loans by raising interest rates where possible. Hence consumer credit and commercial and industrial loans made by commercial banks (as seen on page 2) decline as the consumer deleverages (see page 3). The question is: are loans contracting because borrowers wish to pay down loans or because the banks are not willing to extend the bank’s balance sheets. The answer could be one or the other or both. In this case it is both as a lack of bank and financial institutional capital still keeps most commercial banks in a non-lending mode, with over 400 banks on the FDIC list waiting in a queue to be resolved or liquidated.A risk analysis firm, IRA, places the number of commercial banks in failure at over 2,000 out of the total of approximately 8,000 commercial banks as seen on page 4.

THREE PATHS FROM HERE

Observers discuss three possible paths going forward. The first is the typical Post WW II path of accelerating GDP growth and the return to Potential GDP once the turn has occurred as economic growth feeds on itself. The second emphasized the struggle to overcome the debt build up and efforts to reduce debt and replace insolvent banks with banks that meet capital requirements. The third path is this uptick GDP, is nothing more than a head fake, and we will back down into another leg of the recession when additional lending failures can no longer be papered over with loans that require no accounting adjustment to falling collateral or delinquency or to lower market prices.

THE LONG SLOW RECOVERY PATH

The Long Slow Recovery path pays its respects to the implications of the wealth destruction implications as outlined above. In this view GDP struggles to catch-up to Potential GDP because of the very lengthy process of absorbing excess houses, the time required to resolve the insolvent financial institutions and replace them with solvent ones and for the consumer sector to shed its debt overhang. The recapitalization of the “too big to fail” banks occurred quickly with TARP fund, but the great majority of banks are still in “zombie” mode.

The consumer de-leveraging is proceeding slowly as the consumer is shedding debt at the rate of $250 Billion per year whereas the debt was created at the rate of $600 Billion per year. If it took 5 years to build the debt, at the current rate it would take a decade or more to accomplish the deleveraging.

Other mega issues also must be confronted that will slow economic growth, and these include a trade deficit that will not go away so long as US wages are well above emerging market wages, a fiscal deficit out of control and all efforts to control the fiscal deficit will be anti-growth, and the prospect of continuing capital exodus from the US which is well underway. In this view of the future, GDP could grow but not at a sufficient rate to catch up to Potential, leaving a jobless recovery that in itself creates economic uncertainty which constrains spending.

THE “W” RECOVERY OR THE DOUBLE DIP RECESSION

The third among the popular versions of the future would be those who see the “W” recession. That is, the GDP uptick of this quarter will be followed by a double dip recession. The logic of the W, or double dip recession, is we will experience all the above problems in the slow growth path but the still to come additional financial write downs (especially from commercial real estate and the slow motion recognition of residential mortgage defaults and foreclosures from the large excess housing overhang) will continue to neutralize the ability of the commercial banks to put to work the prodigious liquidity supplied by the central bank. Until the banking system is restored to capital compliance there will be no recovery, and without sufficient funding to resolve insolvent banks, regulators will continue to allow and encourage the cooking of the books and pretend the banks are solvent. This is a policy know as “pretend and extend.” This was made official this week rather than chartering new solvent banks without any contingent historical losses that would be capitalized by the market if allowed to be formed. In other words we are heading down the path of Japan’s lost decade of “zombie” banks.

The Typical Post WWII Recovery Path and Financial Market Mania

The recovery in US fixed income and equity pricing thus far in 2009 are shown clearly on pages 5 and 6 of the handout in terms of appreciation of corporate fixed income and the impressive P/E ratios prevailing in the equity market. This leads to an interesting and intriguing question. If the majority of economists see a protracted sub-par GDP growth rate, what scenario are the financial markets pricing?There are many facets to this issue.

First there it seems clear from analysts and market participant’s statements that the projected growth path ahead resembles all other post WWII recoveries: that once a bottom has been established the retracing of GDP back to Potential and corporate earnings growth will accelerate. Why? Well that’s the way it’s been in the past. When pressed for more analytics, much has been made of corporate gains in efficiency from cost cutting in an effort to maintain cash flow and earnings without recognizing there are two sides of that coin. The cost cutting mostly has fallen on labor which in turn puts a dent in income generation and spending.

Other reasons for this occurrence must rest on, at least in the early stages, the realization that the liquidity in the corporate debt market has allowed many firms who can reach the capital markets to refinance their balance sheets. This has allowed the reduction and extension of debt which reduces their immediate vulnerability to soft goods markets and bankruptcy risk.

The Carry Trade or Financial Leverage

Other factors creating the whoosh of the corporate security market advance are the return to the carry trade as the circumstances for a carry trade recovery have been present. The Carry Trade is simply highly leveraged purchases of assets financed by very inexpensive financing terms when large spreads to existing fixed income exist. Once the market settled down after the 2008 crunch, the low volatility also contributed to a willingness to enter into leveraged positions, especially when financed by US Dollar lenders, hence removing foreign exchange risk. The Carry Trade is often undertaken by hedge funds or investment banks. The cheap funding source follows from the exceedingly low short term market interest rates available. One must wonder who the lenders are if commercial banks have hit the wall in terms of lending capability. It seems the Repo market is placing institutional short term funds from endowments, pension funds, insurance companies, etc. at rates near the Fed funds rate on an overnight basis. Hence financial leveraging does not require solvent commercial banks.

Quantitative Fiscal Policy: The Textbook Free Lunch Version

Public policy to extract an economy from a recession predominantly rests on the shoulders of fiscal policy (tax and spend), monetary policy (lend and spend) and foreign exchange management to induce foreign spending for domestically produced goods. These policies to extract the US economy from a recession have reached a dead end. Let’s take these in turn.

It has long been textbook lore that fiscal policy in the form of government spending or a tax refund generated additional private spending and the additional private spending relates to the government spending as the fabled “multiplier” effect. This occurs because one dollar of government spending results in income generation from the production of the goods the government purchases. When the income is distributed to labor, the great majority of the funds are then spent on consumption goods.Since each consumption good purchased creates additional income and, in turn, round after round of additional consumption, the total effect of a Dollar of government spending is some large multiple (perhaps 10 if the only offset is a marginal savings rate of .1) of the government spending.

However economists have found the theory would only work if there are no offsets to this chain reaction. That is, no other negative frictions on spending occur. This is the “free lunch” version of the multiplier, but, in reality for some time, some economists, most notably Robert Barro of Harvard University, have measured the multiplier effect of government spending and found the effects to be considerably smaller. Over the past few decades he estimates the multiplier effect to be .6, which isless than 1. That is, for each net dollar of government spending, the total spending effect generated,including the dollar of government expenditure, is less than the dollar spent by the government.

Fiscal Policy without the Free Lunch: Fiscal Policy Has Reached a Dead End

A multiplier of less than 1 can only happen if there are offsets to government spending. The concept of the offsets reducing the multiplier to even less than 1, in general, are the result of costs being imposed due to the debt financing that made the government spending possible. So what are those effects? Well first, if the government spending is financed with Treasury debt, this necessitates that financial resources be bid away from private use which places upward pressure on borrowing costs and reduced availability of credit that adversely affects, not only the consumer, but also business investment and state and local governments’ spending. Additional offsets to total spending occur when the expansion of the government deficit creates expectation that the government will be forced to eventually balance the fiscal budget and resort to higher taxes, which offsets the propensity to invest and even to consume.

The pressure to raise taxes comes when the market starts to lose confidence in the ability of the government to roll over its larger debt relative to income. That is, sovereign risk begins to be priced into Treasury rates which in turn raises the cost of capital to all private borrowers. For example, this occurred at the end of the Reagan-Bush Presidencies. The attitude of “watch my lips, no new taxes” was disturbing to the credit markets and caused sovereign risk to be priced, which in turn resulted in higher taxes despite the pledge of no new taxes. Similarly last week the Obama administration announced that it will address fiscal fixes. This must be code for raising taxes or selling government assets.

Other offsets to government spending come from the higher debt service costs, especially when the debt is held by foreign entities. Lastly, the market begins to believe that the sale of the added Treasuries can only occur if financed by the central bank known as the monetization of the debt which on the face of it looks to be creating ultimate inflation and higher associated interest rates.

Today all these factors are operating to add a cost to government spending in the form of offsets to private spending to make the government spending policy almost without any effect at all. For example the fiscal year for the government recently ended with a $1.4 Trillion fiscal deficit but yet GDP or total income and spending declined roughly $800 Billion.

No doubt today the effects of government spending are even more muted as recent tax refunds or rebates of taxes previously paid have resulted in the consumer saving virtually every penny of the rebate, resulting in a multiplier of zero.

The Government Debt to Income Ratio is Skyrocketing and Creating Sovereign Risk

While the inability of the government to propel the economy forward due to the offsets to government spending or tax rebates, there is even a greater problem in trying to move the economy forward using fiscal policy that is debt financed. When a dollar is spent a dollar of government debt is created, but the when the income produced is less than a dollar there is a large marginal increase in the government debt to income ratio. In the past fiscal year the US debt to income ratio shot from .84 to over 1. See page 9 of the handout.

For those who examine credit worthiness the debt to income ratio is an important metric, and the US’s debt to income ratio will continue to spiral upward if fiscal multipliers are less than 1. This is the astounding and grave implication from debt financed government spending when the offsets lower the multiplier below 1. Government spending needs to be thought of as investment in income generation,and if the income produced to ultimately pay for the debt is less than the investment, we have found the formula for sovereign default. To make matters worse the political response is let’s do more of it.

Monetary Policy Has Reached a Dead End

During October 2008 at the time of the intense credit meltdown, the Federal Reserve stepped into the markets and made loans to non-member bank financial institutions, corporations and even began purchasing consumer debt derivatives. When the Fed loans or buys financial instruments, the otherside of the Fed’s balance sheet represents how the loans were funded. In this case the funding was secured by currency issuance and member bank deposits both of which satisfy commercial bank liquidity requirements. These counter items to the Fed credit expansion are called the Monetary Base as seen on page 13. The significance of this is that as the result of the Fed supporting credit markets, commercial banks were provided with sufficient liquidity to fund loans in amounts equal to the total of existing GDP spending. Since liquidity is typically the constraint that limits bank lending, it was generally thought in the months following that the Fed had unleashed an inflationary super bubble that would result from all the lending and spending that hypothetically would take place.

While the great expansion in liquidity did not create the lending and spending due to the banks not meeting capital requirements, none-the-less this unleashed inflation expectations of a high order of magnitude. The inflation expectations lead to increasing the interest rate, which is the last thing the Fed wished to see in a serious recession. To counter this adverse perception, the Fed announced its intention to “exit” the market early last summer. This had the intended effect of reducing inflation expectations and interest rates came down as a result, but it did serve to make clear to the Fed that the market would not tolerate any further increase in its balance sheet. Also, the Fed had to backtrack on its original announcement that it would finance near a Trillion Dollars of the Federal deficit and instead put the Treasury on a “budget” of $300 Billion for this year. Clearly the Fed has hit the limit of how much money it can infuse in the banking system without adverse market tolerance. The Fed is up against the wall and will likely need to make good on “exiting”, whatever that will mean.

Exchange Rate Policy has Reached a Dead End

China has been intervening in the foreign exchange market to prevent her currency appreciation when she runs a trade surplus and is the beneficiary of capital inflows as well. In turn many countries who compete with China feel to remain competitive they also must sell their currency vs. the dollar to keep it from appreciating and still be able to compete with China in the export markets. Furthermore, Brazil has just announced a tax on capital imports to restrain the effects of said capital inflows in its currency value. All these foreign exchange interventions are designed to keep Emerging Nation currencies cheap relative to the US Dollar. All this intervention supports the dollar and prevents the US Dollar and US goods from being competitive in world markets.

Now if the US decided it could play the same game and sell its currency to cheapen the dollar to encourage exports and a US economic recovery (which it hypothetically could do), there are constraints from carrying this out. The major constraint is the US is foreign capital dependent to fund its fiscal deficit, and intentionally driving down its currency will drive out not only future capital inflows but would encourage the $6 Trillion net debts with the rest of the world to pull out of the Dollar.

The US dead end in exchange rate policy comes from this clash of objectives. A cheap dollar to encourage exports would drive away scarce capital and cause the US Dollar to more quickly surrender its reserve currency status.

Policy Alternatives

The policy alternatives not being considered actively are those that are somewhat “out of the box.”They are decidedly not the standard macroeconomic recovery tools which we have previously discussed which are not effective in a debt ridden deflationary economy. First, one would need to recognize that consumer insolvency is de facto widespread though unresolved and the same can be said for financial institutions generally. The resulting no-spend, no-lend prevents any stimulus, whetherfiscal or monetary, to be effective in combating the imbalance that exists. There are a few courses of action however. Basically they are efforts to either inflate asset prices or reduce debt.

The first would be to restore housing prices which would have a positive wealth effect on the consumer, and it would give greater value to mortgage debt which is collateralized by houses. This in turn would restore financial institution asset values that in turn would effectively recapitalize banks.There would be no need or considerably less need of public capital infusions via TARP, less need to close banks, and less need for a private recapitalization of the banking sector.

How might this be accomplished simply is through reducing housing supply. At this point approximately $300 billion of TARP funds have been repaid which could provide the funding to purchase approximately 3 million or half of the housing overhang from banks as they are foreclosed and then demolished them.This contraction in supply would bring about a restoration in housing prices and in mortgages and residential mortgage backed securities as the collateral behind the mortgages are restored in value.While this is fundamental economics, it flies in the face of a moral sense that while public funds are generally spent with little to show in terms of welfare, this would seem to be an over-the-top outrage,as it explicitly makes the statement that government spending undermines welfare. However, the program could be carried out as a “condemnation” policy as these empty houses have menacing neighborhoods effects.

Another possible way to appreciate assets is the original TARP idea, which proved to be require a much large capital purchases program than what was funded. An indirect way though has been found by lowering interest rates to the point where the carry trade is inflating most but not all asset categories.

Another way to accomplish the goals of reducing debt and add to the value of assets is to have a purposeful inflation, that is, inflation by design. The purpose of this would be to devalue the over-indebtedness in real terms and cause the market to run to housing as an inflation hedge. This would eliminate the common problem of consumers being “upside down.” While the Fed can’t create inflation via consumer spending currently, inflation by design could be carried out by the Treasury taking the Fed under its wing as has been done before in WWII (The Accord) and effectively in the Civil War (The Fed didn’t exist at that time) with the Treasury printing currency to pay the government’s bills. This did the trick of creating market demand out of new money issued that was inflation-generating.

Lastly, national debt forgiveness, that is a debt cram down, is a desirable alternative to reduce private indebtedness. Doing this quickly by legislation is superior to the long and drawn out and costly individual bankruptcy process that accomplishes the same result but at a much higher transaction cost in terms of lengthening a recession with greater income loss. This is also superior to a private effort to deleverage that has produced perhaps $500 billion of reduced debt by consumers and businesses in the last year but at the cost of increasing national debt by $1.4 Trillion.

Economic growth in the developed world is falling well short of the post-WWII experience, and there are identifiable causes.

Economic growth in the developed world is falling well short of the post-WWII experience, and there are identifiable causes.

Economic regulation and its counter-effect on economic growth — a rising background issue until now — has just vaulted to the front pages with President Obama’s recent speaking tour, signaling a redirection of policies and mischief ahead.

Economic regulation and its counter-effect on economic growth — a rising background issue until now — has just vaulted to the front pages with President Obama’s recent speaking tour, signaling a redirection of policies and mischief ahead. commercial bank cash reserves are sitting on deposit at the Fed rather than being loaned out. While indeed there are other causes as well for the unloaned cash accumulation in commercial banks, financial regulation is under-rewarded for praise.

commercial bank cash reserves are sitting on deposit at the Fed rather than being loaned out. While indeed there are other causes as well for the unloaned cash accumulation in commercial banks, financial regulation is under-rewarded for praise. A printing press is a handy thing to have. When a government or central bank can fund itself with money or claims on money, it can buy a lot of things and solve a host of problems, all without the need to tax. I wish I had one.

A printing press is a handy thing to have. When a government or central bank can fund itself with money or claims on money, it can buy a lot of things and solve a host of problems, all without the need to tax. I wish I had one. So as we approach the target unemployment rate without much economic recovery, the question is, can and will the target be redefined to be the unspoken necessity of supporting Treasury debt obligations?

So as we approach the target unemployment rate without much economic recovery, the question is, can and will the target be redefined to be the unspoken necessity of supporting Treasury debt obligations?  Today there is a de facto peg already in place. It goes under the title of zero interest rate policy (ZIRP). It is also known as financial repression, which includes ZIRP along with positive inflation causing real yields to go negative all the way out to almost 20 year maturities and has become the explicit policy of the Japan and implicitly of Europe as well.

Today there is a de facto peg already in place. It goes under the title of zero interest rate policy (ZIRP). It is also known as financial repression, which includes ZIRP along with positive inflation causing real yields to go negative all the way out to almost 20 year maturities and has become the explicit policy of the Japan and implicitly of Europe as well. income over the same period, transfer payments by governments as a share of the income pie has increased by 10 percentage points, as shown in the accompanying graph.

income over the same period, transfer payments by governments as a share of the income pie has increased by 10 percentage points, as shown in the accompanying graph. ability to continue compensating for the loss of wage income by borrowing and transferring has hit up against funding limits due to baby boomer entitlements coming due. The cookie is crumbling, but the election indicates the middle class still wants its cookie — and the ability to borrow someone else’s cookie and pass it around has reached an un-financeable end. We have three choices: take a cookie from “rich folks” and pass it around, grow the number of cookies, or realize there will be fewer cookies. The redistribution argument won at the ballot box.

ability to continue compensating for the loss of wage income by borrowing and transferring has hit up against funding limits due to baby boomer entitlements coming due. The cookie is crumbling, but the election indicates the middle class still wants its cookie — and the ability to borrow someone else’s cookie and pass it around has reached an un-financeable end. We have three choices: take a cookie from “rich folks” and pass it around, grow the number of cookies, or realize there will be fewer cookies. The redistribution argument won at the ballot box.

These are complicated times, especially when it comes to inflation.

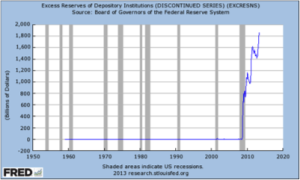

These are complicated times, especially when it comes to inflation. banking system did not have the requisite regulatory solvency (an excess of asset values relative to deposits) to expand balance sheets if they had the risk tolerance. That is, today’s excess cash reserves of $1.5 trillion held by banks and a commercial bank money supply multiplier of say 10 would normally result in $15 trillion of lending and spending. A surge in bank-financed spending could roughly double the present $15 trillion annual flow rate of GDP and, with it, inflation.

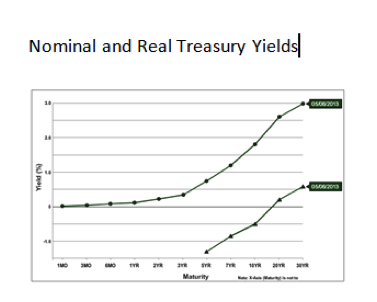

banking system did not have the requisite regulatory solvency (an excess of asset values relative to deposits) to expand balance sheets if they had the risk tolerance. That is, today’s excess cash reserves of $1.5 trillion held by banks and a commercial bank money supply multiplier of say 10 would normally result in $15 trillion of lending and spending. A surge in bank-financed spending could roughly double the present $15 trillion annual flow rate of GDP and, with it, inflation. And some believe it will keep going. The price of the U.S. Treasury 10-year bond recently reached an all-time high, generating yields at all-time lows. Moreover, the market yield on the British perpetual bond is reportedly at a 300-year low. Bond mania has even spread to the sovereign debt of Denmark and Singapore and others where negative yields exist. More astonishing is the ability of France to issue short-term sovereigns with negative yields!

And some believe it will keep going. The price of the U.S. Treasury 10-year bond recently reached an all-time high, generating yields at all-time lows. Moreover, the market yield on the British perpetual bond is reportedly at a 300-year low. Bond mania has even spread to the sovereign debt of Denmark and Singapore and others where negative yields exist. More astonishing is the ability of France to issue short-term sovereigns with negative yields! Depression era came to an end with the onset of World War II, as shown in the chart to the right.

Depression era came to an end with the onset of World War II, as shown in the chart to the right. (That being said, it leaves open the question of whether intentional inflation is bravado in the absence of bank lending, which will be addressed in a subsequent blog.)

(That being said, it leaves open the question of whether intentional inflation is bravado in the absence of bank lending, which will be addressed in a subsequent blog.) its member governments “are facing unprecedented

its member governments “are facing unprecedented