2009 Financial Market Trends

In the last month of 2009 some of the financial trends of the year seemed to veer off course. While trend reversal in December is not unexpected as money managers seek to realize and book audacious total returns to give them bragging rights for their 2009 performance, however, the recent retreat on a number of fronts raises the question of whether the underlying expectations that drove asset performance in 2009 are changing. If that is the case expect 2010 to be different.

The year was dominated by the rush into US and emerging country risk assets along side of a rush out of the US Dollar and into commodities and commodity currency investments. What seems clear is there were three major expectations (not likely by the same group of investors) that moved financial markets and total returns in 2009. First, the US economy would spring back, otherwise known as the “V” recovery, which drove US risk assets, both debt and equity, upwards. The second expectation being priced was the idea that emerging markets (EMs) and especially China among the EMs would grow and prosper even if the US and the developed world might not, again pushing upward both debt and equity in those countries.

A third expectation that moved some investors is the realization that the US is in a very deep fiscal hole that we keep digging ever deeper as there is no politically feasible exits from entitlement program spending. The forward looking US fiscal deficit produces genuine fears of an ultimate US Treasury default when the market becomes unwilling to roll over Treasuries in which case it is presumed that the US Dollar printing press would be employed to make good on US obligations. Hence US sovereign risk and inflation risk is the flip side of the same coin that produced strong movements away from the US Dollar and into commodity hedges especially gold and commodity currency investments.

The not unrealistic expectation of the long term US fiscal malaise provided the spark behind the broad based desire to be out-of-the US Dollar which resulted in a decline of 15% in the US Dollar at its peak in 2009 (despite Dollar support by some of the EMs), a rush into commodities despite the weak end use of commodities, especially oil, and a desire to reallocate capital from the US to the EMs. This US fiscal/inflation related risk also tended to produce a steep yield curve and a preference for TIPs over long term fixed rate debt.

The 2009 asset class performance was also influenced by the basic economics of the Carry Trade which was funded by almost costless leverage available in the US Repo market. With cheap short term credit available in the US which in turn funded leveraged acquisitions of fixed income in other lands in order to gain spread income helped push along the uptrend in risk assets generally but especially in the EMs and pushed down the US Dollar as funds borrowed in the US were invested offshore.

Credit Problems Abroad and a Flight Back to the Dollar?

The basis for possibly believing that asset class performance will be different in 2010 comes from new developments as the economic crisis/recovery morphs along. The first challenge to the V recovery is the realization that the Fed is under pressure to produce the “exit” from financial markets that it has promised and the economic recovery (x-government steroids) is still weak despite continued fiscal and monetary injections. Though the US growth picture will perk up this quarter due to a strong inventory build-up for Christmas, but it is far from clear that a deleveraging consumer without a commercial bank capacity and willingness to lend will actually produce a V recovery equal to that which has been priced in and additionally we face the prospects of growth killing tax increases to help control the US fiscal deficit.

Another challenge to the market pricing of the V recovery comes from skeptics who see economic malaise in 2010 and forward years based on renewed loan losses from commercial real estate and private equity loans that can’t be totally covered up with accounting obfuscation and de facto suspension of bank closure. The double dip expectation was no doubt stimulated by the Dubai state run real estate empire defaults. So as we near the end of 2009, current developments are curiously reinforcing both the V and the W enthusiasts. Though both can’t be right simultaneously, the expectations can simultaneously be held by different groups of investors at the same time and move different assets classes consistent with this mutually exclusive thinking. In this case an actual double dip recession or W recovery would cause related risk assets such as commercial mortgage securities to weaken as well as the banks that are holding them.

Another important change that is taking place is the rebound in the US Dollar What might be causing the US Dollar rebound is NOT a change in the long term US fiscal threat except for the resistance to further fiscal red ink now taking hold in Congress but a new event has highlighted the possibility that while our LONG term fiscal problems are dire, there are other countries with even more dire SHORT term problems that will cause funds to flow back into the Dollar and from there into the Treasury market as the RELATIVELY safe haven for wealth at least for now — much as occurred in 2008.

Specifically the UK and a variety of Euro zone country debt is now under the market microscope. These European countries for which fiscal deficits are more out of control than the US, their sovereign debt has been downgraded or is under review are now paying up to 250 basis points of sovereign risk premiums on ten year paper relative to the German Bund. Those hardest hit are appropriately known as the PIGS (Portugal,Ireland,Greece and Spain). The PIGS make the US look attractive if only by comparison causing funds to shift to the US Dollar/Treasury trade so the US dollar is now appreciating relative to the Euro breaking the Dollar down and Gold and EM currencies up momentum in their tracks.

Losses in the market value of European sovereign debt as well as the Dubai debt write downs in turn weaken European banks and in turn the European economy already fighting their trade problems with an appreciated Euro when capital fled from the US Dollar. The Dubai real estate based default that is trickling down to European financing banks is a reminder of the contagion that can be unleashed from seemingly isolated credit defaults (as with the subprime residential mortgage securities).

The Dubai credit event also brings back to center stage the fear that banking system will need to digest further commercial real estate and private equity loan losses for loans that mature between 2010 to 2014 without government backstops. That is, banking systems are now more vulnerable not just due to its book of loans but the effective removal of government financial back up due to the moral outrage that followed the repayment of TARP funds. That is, not many politicians will likely vote for TARP II if needed. The Dubai and the Euro sovereign debt risks remind us that we are not out of the woods of bank insolvencies, credit meltdowns which might account for the recent reversal in the market pricing of financials.

The credit problems of Dubai, the UK and the PIGS are not isolated events in that each has strong reverse momentum effects on the Dollar and commodities as each of these trades has heavy option positions betting their continuation. Hence if the price movement is reversed they will both be potentially subjected to significant trend reversal when the respective Dollar shorts and gold and commodity long positions must be covered. (See David Rosenberg,https://ems.gluskinsheff.net/Articles/Breakfast_with_Dave_121509.pdf ). Furthermore even greater threats to a correction from 2009 asset performance is possible because the Carry Traders are incented to unwind their carry positions financed from US Dollar sources when the Dollar is appreciating.

Hence, if the credit shocks in Europe gives the US Dollar/Treasury a new lease on life as the financial system’s flight to quality asset and elevates their prices, the carry trader who borrowed in the US and in turn sold dollars to be holding commodity currencies now have greater incentives to unwind their now riskier and potentially loosing bets if the correction in the US Dollar continues. A collapse of the carry trade will add to dollar demand and will further elevate the US dollar just as it contributed to its decline in 2009. It will also bring the commodity boom and gold boom under control.

These forces now favoring the US dollar have mixed effects on the V recovery. Foreign capital keeps interest rates low even if the Fed “exits” but it also removes some favorably V momentum in that we were just beginning to feel the benefits of a cheaper Dollar. Other countries were starting to outsource their production to the US given its relatively cheaper currency (e.g. Mercedes and Toyota).

All in all, foreign capital favoring your economy is a lucky reprieve in the third year of the Great Recession. The question remains will the actual V be up to the standards that have already been priced into the market.

If there is a shift in preference away from European and Middle East risk to the US Dollar/Treasury as the flight to quality asset, this generates significant shock waves to the price trends of 2009 created from the expectation of US sovereign default. On the other hand it could be on balance favorable to those betting on the V recovery and on those emerging nations that can grow on their own, with China the most obvious candidate.

Hence 2010 has the potential to experience Dollar strength and commodity weakness. In a sense we have caught a break from our fiscal troubles of financing the US deficit for a while but ultimately they are still there. Looking at the positive side of these developments, it looks like a buying opportunity is being created in foreign currency investments for countries that do not have acute fiscal problems.

And some believe it will keep going. The price of the U.S. Treasury 10-year bond recently reached an all-time high, generating yields at all-time lows. Moreover, the market yield on the British perpetual bond is reportedly at a 300-year low. Bond mania has even spread to the sovereign debt of Denmark and Singapore and others where negative yields exist. More astonishing is the ability of France to issue short-term sovereigns with negative yields!

And some believe it will keep going. The price of the U.S. Treasury 10-year bond recently reached an all-time high, generating yields at all-time lows. Moreover, the market yield on the British perpetual bond is reportedly at a 300-year low. Bond mania has even spread to the sovereign debt of Denmark and Singapore and others where negative yields exist. More astonishing is the ability of France to issue short-term sovereigns with negative yields! Depression era came to an end with the onset of World War II, as shown in the chart to the right.

Depression era came to an end with the onset of World War II, as shown in the chart to the right. (That being said, it leaves open the question of whether intentional inflation is bravado in the absence of bank lending, which will be addressed in a subsequent blog.)

(That being said, it leaves open the question of whether intentional inflation is bravado in the absence of bank lending, which will be addressed in a subsequent blog.)

The financial press’s take on the economy and financial markets has lately been cloudy. The growth rate has indeed been drifting and the economy is being subjected to adverse shocks. But let me suggest there is good reason to believe there is a positive direction emerging below the radar of the cross-currents.

The financial press’s take on the economy and financial markets has lately been cloudy. The growth rate has indeed been drifting and the economy is being subjected to adverse shocks. But let me suggest there is good reason to believe there is a positive direction emerging below the radar of the cross-currents.

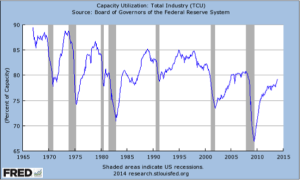

Furthermore, most of our emerging market competitors’ utilization rates are above those of the U.S., so the expansion of the capital goods industries is likely to be a global phenomenon.

Furthermore, most of our emerging market competitors’ utilization rates are above those of the U.S., so the expansion of the capital goods industries is likely to be a global phenomenon. income over the same period, transfer payments by governments as a share of the income pie has increased by 10 percentage points, as shown in the accompanying graph.

income over the same period, transfer payments by governments as a share of the income pie has increased by 10 percentage points, as shown in the accompanying graph. ability to continue compensating for the loss of wage income by borrowing and transferring has hit up against funding limits due to baby boomer entitlements coming due. The cookie is crumbling, but the election indicates the middle class still wants its cookie — and the ability to borrow someone else’s cookie and pass it around has reached an un-financeable end. We have three choices: take a cookie from “rich folks” and pass it around, grow the number of cookies, or realize there will be fewer cookies. The redistribution argument won at the ballot box.

ability to continue compensating for the loss of wage income by borrowing and transferring has hit up against funding limits due to baby boomer entitlements coming due. The cookie is crumbling, but the election indicates the middle class still wants its cookie — and the ability to borrow someone else’s cookie and pass it around has reached an un-financeable end. We have three choices: take a cookie from “rich folks” and pass it around, grow the number of cookies, or realize there will be fewer cookies. The redistribution argument won at the ballot box.