Bonds are fun to own when interest rates are very high and then bond prices start to rise. That simultaneously makes for favorable income and capital gains. Such was the opportunity bond investors in U.S. markets enjoyed commencing in 1981 … and then for three more decades until recently. It was Bond Market Nirvana, which unfortunately for investors is fading into the rear view mirror.

Bonds are fun to own when interest rates are very high and then bond prices start to rise. That simultaneously makes for favorable income and capital gains. Such was the opportunity bond investors in U.S. markets enjoyed commencing in 1981 … and then for three more decades until recently. It was Bond Market Nirvana, which unfortunately for investors is fading into the rear view mirror.

The anomalous double-dipping of both high-yielding checks in the mail and capital appreciation was due to a favorable confluence of macroeconomics.

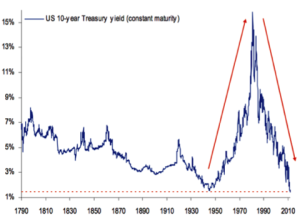

Nirvana first required bonds to be extraordinary cheap as an entry point, and the rising energy-related inflationary pressures of the 1970s created that condition. Bond prices became dirt cheap at the end of that decade, making for sky-high (historic) yields, as the accompanying graph depicts.

What set up the entry point for Bond Nirvana was the bond market flight that preceded it. Then when the inflationary environment was replaced by persistent disinflation as the result of ongoing emerging nation competition, it caused investors to return to a bond market opportunity, not just of a generation but in the history of the Republic. The graph reveals no higher highs in interest rates than in 1981 and no greater sustained plunge of rates caused by the rise in the secondary market value of bonds.

What set up the entry point for Bond Nirvana was the bond market flight that preceded it. Then when the inflationary environment was replaced by persistent disinflation as the result of ongoing emerging nation competition, it caused investors to return to a bond market opportunity, not just of a generation but in the history of the Republic. The graph reveals no higher highs in interest rates than in 1981 and no greater sustained plunge of rates caused by the rise in the secondary market value of bonds.

The favorable bond environment persisted because business conditions were sufficient to marginalize default possibilities with but a few cyclically correcting deviations. But more importantly, through most of the Nirvana period, there were foreign capital inflows to the U.S. associated with globalism, and foreign capital was parked in U.S. marketable debt.

Another development in the later stages of the three-decade run was the invention of the shadow banking system, in which very cheap short-term financing was available for some investors (hedge funds, for example) to leverage up on the higher-yielding and appreciating bonds.

But about 26 years into Nirvana, it was propelled into another major upward spike.

As a response to the financial and economic crisis of 2007-08, the Fed began a bond buying program not in the tens of billions as before, but in the trillions of dollars — and with that much buying power in the bond market, prices were driven to an even higher plateau.

And on top of propelling Nirvana, the Fed’s purchase of U.S. bonds provided more spending power to those selling their bonds to the central bank, thus allowing them to purchase higher-yielding bonds — many of which were from offshore markets. This in turn caused foreign central banks across the globe (including developed-world central banks) to purchase U.S. assets in order to control their currency appreciation (by selling their currencies for U.S. assets).

Aside from the favorable macro-environment for bonds, there were regulatory and behavioral factors that favored bonds as an investment class, which added further fuel to Bond Market Nirvana.

After three decades of persistent and consistent positive returns to both current income and appreciation, bonds became not just an investment class for regulatory constrained financial institutions whose portfolios required bond exclusivity, but also an attractive option for investors enamored with the income and appreciation bonds provided — and why not? After three decades of success, too many projected it to be a permanent financial gimme, and they still do.

In the ascendancy of bond Nirvana, the primary beneficiaries were financial institutions and pension funds that by regulation or self-imposed rules of allocation were required to own bonds as a substantial portion of their asset portfolios. Indeed, it was a wealth windfall to financial institutions, and the equity price of the financial sector outperformed the industrial and trade sectors for some time.

So bond-oriented investment managers, either by orientation or inclination, went public to the retail market, and their clients enjoyed the run as well via bond mutual funds and ETFs.

The name most associated with this success is Bill Gross of PIMCO, who became known  as the “Bond King,” though there are others as well.

as the “Bond King,” though there are others as well.

But when the juggernaut reached its ultimate ascendancy, bond prices were historically elevated and interest yields were at the Republic’s lowest. This a piece of history likely concluded in August 2012.

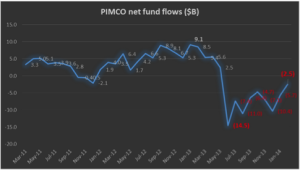

One can only make an educated guess that there must have been great stress in the Bond King’s world as cracks in the facade of effortless investing brilliance revealed the boom to be dependent on macroeconomic tailwinds. In 2013 these bond-oriented clients took a loss of 3.7%, which is relatively small compared to stock market volatility. But as a result, the bond fund suffered a 14.4% redemption rate by those surprised clients who did not receive their accustomed appreciation. Indeed, the vulnerability was great enough to cause four times the rate of redemptions as compared to investors’ annual losses — a ratio that no money manager can long sustain.

Since investment management is paid according to money under management, there was consternation in bond land, and someone needed to be found guilty. As one could expect there was a high profile resignation at the co-CEO level, a shakeup in top management, and statements of client caring and diligence ahead. Indeed, PIMCO and all other bond specialists are fighting an uphill battle and need to reassure investors, lest there are any more defections from the USS PIMCO and Bond land in general.

And there is lots of bravado in PIMCO’s online commentary, in which it pledges to navigate the market change without changing course! There are actually cracks and crevices in which to seek shelter from the bond market fallout, and they pledge active management, but they are on the slippery downward slope and they know it.

As far as their investors are concerned, they need to realize that the income received from their interest payments do not cover the losses in market value of their bonds. Basically, they are consuming their capital when they receive their periodic interest payments.

PIMCO said it all in a recent online posting in which it warned investors that “a high allocation to U.S. Treasuries, which are more sensitive to changes in interest rates … may have poor growth prospects due to an unhealthy balance sheet” — I presume of the U.S. government, not theirs. Ironically the bond losses would be greater for Treasuries at the same maturity than bonds of all pedigree, including Muni’s, but bond losses nonetheless are on the horizon.

Actually, the end of Bond Nirvana does indeed relate to the increasingly poor shape of the U.S. balance sheet better known as pricing-in sovereign risk — but it is also happening because the long wait for a deflation to make the bonds more valuable in the market has not occurred. There is also good reason to believe that mildly increasing inflation is in our future despite inflation softening in Europe.

This is based on a growing effective labor shortage and a still-expanding economy despite the winter’s weather-related slowdown. And then there is minimum wage legislation and executive orders regarding overtime pay that ratchet up wages and, in turn, business costs and prices.

But that is not all that threatens Bond Nirvana. The other basic tenants of Bond Nirvana are also crumbling. The foreign trade surpluses to the U.S. are shrinking, causing a slowdown in foreign accumulation of dollars and bonds. Furthermore, the shadow banking system of financial leverage (think hedge funds) will be constrained when short-term interest rates rise.

And there is now a new counter-force to Bond Market Nirvana. The U.S. is now actively looking to impose “financial constraints” on countries that do not follow our foreign policy (in this case, Russia). By seizing or freezing foreign assets and making access to the dollar payment system off limits to those we seek to discipline, our government will cause foreign capital to move to another currency and another country quickly. Indeed, foreign central banks’ holdings of U.S. Treasuries — with the U.S. Federal Reserve acting as custodian — had record withdrawals immediately. We are on a new global control path that will have adverse consequences to the foreign holding of U.S. bonds and to Bond Nirvana.

And then there is tapering — not just by the Federal Reserve but also by the emerging nations that are being hit hard by the taper and selling their dollar investments in order to support their own currencies. And recently, the Fed let the cat out of the bag and let it be known that increases in short term policy rates are on the horizon.

Altogether, these forces are too powerful for one to believe that Bond Nirvana is not in the rearview mirror. Indeed, such a large deviation from financial norms as Bond Nirvana required a number of simultaneous moving parts to create such an epic market opportunity.

Though favorable expectations and the bond reflex are still strong after such a long reinforcing run, there is too much going against the trend for investors to think they can rely on it in the future.

Bond Market Nirvana is one for the history books on the scale of a 300-year flood, but alas income and growth can be found elsewhere in the growing sectors of the economy, though regrettably not on the scale of Bond Nirvana.

Sign up to receive the Spellman Report. Bracing financial and economic insight. Now with free delivery!

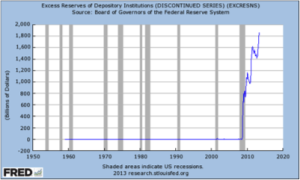

Economic regulation and its counter-effect on economic growth — a rising background issue until now — has just vaulted to the front pages with President Obama’s recent speaking tour, signaling a redirection of policies and mischief ahead.

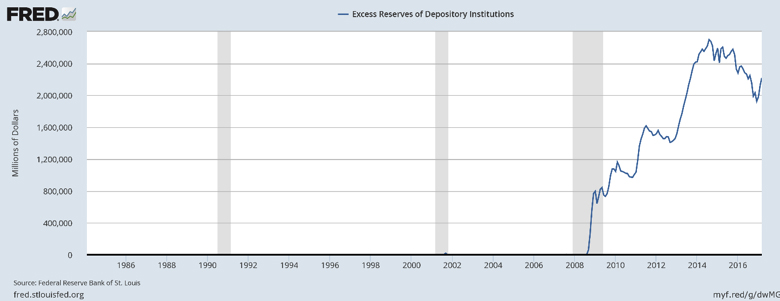

Economic regulation and its counter-effect on economic growth — a rising background issue until now — has just vaulted to the front pages with President Obama’s recent speaking tour, signaling a redirection of policies and mischief ahead. commercial bank cash reserves are sitting on deposit at the Fed rather than being loaned out. While indeed there are other causes as well for the unloaned cash accumulation in commercial banks, financial regulation is under-rewarded for praise.

commercial bank cash reserves are sitting on deposit at the Fed rather than being loaned out. While indeed there are other causes as well for the unloaned cash accumulation in commercial banks, financial regulation is under-rewarded for praise.